Advantage India

Robust

Demand

*As per the Insurance Regulatory and Development Authority of India (IRDAI), India will be the sixth-largest insurance market within a decade, leapfrogging Germany, Canada, Italy and South Korea.

*The regulatory developments would furthermore contribute to the growth.

*The recent pandemic has emphasized the importance of healthcare on the economy, and health insurance would play a critical role in the effort to strengthen the healthcare ecosystem.

Attractive

Opportunities

*Insurance market in India is expected reach US$ 222 billion by 2026.

*Robotic Process Automation (RPA) and AI will occupy center stage in insurance, driven by newer data channels, better data processing capabilities and advancements in AI algorithms.

*Bots will become mainstream in both the front and back-office to automate policy servicing and claims management for faster and more personalized customer service.

Policy

support

*The government’s flagship initiative for crop insurance, Pradhan Mantri Fasal Bima Yojana (PMFBY), has led to significant growth in the premium income for crop insurance.

*Ayushman Bharat (Pradhan Mantri Jan Arogya Yojana) (AB PMJAY) aims at providing a health cover of 5 lakh per family per year for secondary and tertiary care hospitalization.

*Insurance cover for 44.6 crore persons under PM Suraksha Bima and PM Jeevan Jyoti Yojana was provided during the FY23.

Increasing

Investments

* As announced in November 2023, Zurich Insurance Group is set to acquire a majority stake in Kotak General Insurance, marking the first major foreign investment in India's insurance sector in eight years.

* The IPO of LIC of India was the largest IPO ever in India and the sixth biggest IPO globally in 2022.

Introduction

India’s Insurance industry is one of the premium sectors experiencing upward growth. This upward growth of the insurance industry can be attributed to growing incomes and increasing awareness in the industry. India is the fifth largest life insurance market in the world's emerging insurance markets, growing at a rate of 32-34% each year. In recent years the industry has been experiencing fierce competition among its peers which has led to new and innovative products within the industry. Foreign Direct Investment (FDI) in the industry under the automatic method is allowed up to 26% and licensing of the industry is monitored by the insurance regulator the Insurance Regulatory and Development Authority of India (IRDAI).

The insurance industry of India has 57 insurance companies - 24 are in the life insurance business, while 34 are non-life insurers. Among the life insurers, Life Insurance Corporation (LIC) is the sole public sector company. There are six public sector insurers in the non-life insurance segment. In addition to these, there is a sole national re-insurer, namely General Insurance Corporation of India (GIC Re). Other stakeholders in the Indian Insurance market include agents (individual and corporate), brokers, surveyors and third-party administrators servicing health insurance claims.

The insurance industry has undergone numerous transformations in terms of new developments, modified regulations, proposals for amendments and growth in 2022. These developments have opened new avenues of growth for the industry while ensuring that insurers stay relevant with changing times and the latest digital disruptions.

The Insurance Regulatory and Development Authority India (IRDA) is vigilant and progressive and is determined to achieve its mission of ‘Insurance for all by 2047’, with aggressive plans to address the industry’s challenges.

The growth of the insurance market is being supported by important government initiatives, strong democratic factors, conducive regulatory environment, increased partnerships, product innovations, and vibrant distribution channels.

Insurance Industry was largely dominated by offline channels like corporate agents, offline brokers or banks. Today, rapid digitization, product innovation and progressive regulation policies have made it possible for consumers to buy insurance through multiple distribution channels with the click of a button. The instability of the covid-19 pandemic highlighted the necessity for consumers to invest in products that would increase financial security, one of them being life insurance.

Market Size

The insurance industry in India has witnessed an impressive growth rate over the last two decades driven by the greater private sector participation and an improvement in distribution capabilities, along with substantial improvements in operational efficiencies.

In FY24 (until September 2023), non-life players’ saw a premium income increase by 14.86% year-over-year to Rs. 1,43,802 crore (US$ 17.29 billion) due to strong demand for health and motor policies.

The Indian non-life insurance industry logged 14.86% growth during the first half of FY24 as compared to 15.30% growth for the same period the previous year. The business growth for the first half of FY24 was driven by health (especially the group segment), motor, and crop insurance.

In April-November 2023, life insurers’ new business premiums grew to Rs. 211,690.65 crore (US$ 25.38 billion), according to Life Insurance Council data.

The premium in the month of March 2023 for the private life insurance industry grew at a healthy pace of 35% on a year-on-year basis and 20% for FY23.

Life insurance firms collected 18% more premiums in FY23 compared to the year before. Life insurers collected Rs. 3.71 lakh crore (US$ 44.85 billion) as the first-year premium in FY23 as against Rs. 3.14 lakh crore (US$ 37.96 billion) in FY22, shows the latest IRDAI data.

Mr. Debashish Panda, Chairman, IRDAI informed that the insurance industry of India has become a Rs. 59 crore (US$ 7.1 million) industry as of February 2023.

Driven by a pick-up in health and motor insurance segments, the non-life insurance industry has grown by 16.4% in FY23 compared to 11.1% in the previous year.

Among the private players, SBI Life, HDFC Life and ICICI Prudential Life led the industry in premium collection. SBI Life collected Rs. 29,587 crore (US$ 3.57 billion) premium in FY23 while HDFC Life and ICICI Prudential Life received Rs. 28,876 crore (US$ 3.48 billion) and Rs. 16,921 crore (US$ 2.04 billion), respectively.

As expected, the state-run insurance behemoth LIC alone contributed over 60% to the total new business premium collection. The insurer received close to Rs. 2.31 lakh crore (US$ 27.93 billion) as premium in FY23 compared to Rs. 1.99 lakh crore (US$ 24.06 billion) in FY22.

Among the private players, SBI Life, HDFC Life and ICICI Prudential Life led the industry in premium collection. SBI Life collected Rs. 29,600 crore (US$ 3.58 billion) premium in FY 2023 while HDFC Life and ICICI Prudential Life received Rs. 28,900 crore (US$ 3.49 billion) and Rs. 17,000 crore (US$ 2.05 billion), respectively.

According to the latest data released by the insurance regulator – the Insurance Regulatory and Development Authority of India - LIC improved its market share by 67.72% as of October, a gain of 447 basis points (bps). At the end of 2021-22, private players had a 36.75% share of the life insurance market, while LIC had 63.25%.

With nearly 62.58% of the new business market share in FY23, Life Insurance Corporation of India, the only public sector life insurer in the country, continued to be the market leader.

In FY23, non-life insurers (comprising general insurers, standalone health insurers and specialized insurers) recorded a 16.4% growth in gross direct premiums.

In India, gross premiums written off by non-life insurers reached US$ 10.95 billion in FY24* and US$ 31 billion in FY23.

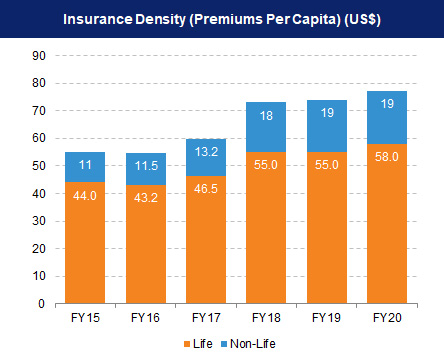

The life insurance industry was expected to increase at a CAGR of 5.3% between 2019 and 2023. India’s insurance penetration was pegged at 4.2% in FY21, with life insurance penetration at 3.2% and non-life insurance penetration at 1.0%. In terms of insurance density, India’s overall density stood at US$ 78 in FY21.

Premiums from India’s life insurance industry is expected to reach Rs. 24 lakh crore (US$ 317.98 billion) by FY31.

Between April 2021-March 2022, gross premiums written off by non-life insurers reached Rs. 220,772.07 crore (US$ 28.14 billion), an increase of 11.1% over the same period in FY21. In May 2022, the total premium earned by the non-life insurance segment stood at Rs. 36,680.73 crore (US$ 4.61 billion), a 24.15% increase compared to the previous year’s period. The market share of private sector companies in the general and health insurance market increased from 48.03% in FY20 to 49.31% in FY21 to 62.5% in FY23. Six standalone private sector health insurance companies registered a jump of 66.6% in their gross premium at Rs 1,406.64 crore (US$ 191.84 million) in May 2021, as against Rs. 844.13 crore (US$ 115.12 million) earlier.

According to S&P Global Market Intelligence data, India is the second-largest insurance technology market in Asia-Pacific, accounting for 35% of the US$ 3.66 billion insurtech-focused venture investments made in the country.

Investments and Recent Developments

The following are some of the major investments and developments in the Indian insurance sector.

- As announced in November 2023, Zurich Insurance Group is set to acquire a majority stake in Kotak General Insurance, marking the first major foreign investment in India's insurance sector in eight years.

- As announced in June 2023, Go Digit Life Insurance, in which both HDFC Bank and Axis Bank have bought stakes, plans to invest Rs. 500-600 crore (US$ 60.3-72.4 million) in the initial 18 months to start out as the country's 26th life insurer.

- As informed in September 2023, the UK and India have agreed to launch a partnership to boost cross-market investment by the insurance and pension sectors.

- In August 2023, Tata AIA launched a ULIP plan with benefits of critical illness cover- Tata AIA Pro Fit.

- With the introduction of new private sector companies, the insurance sector in India gained momentum in the year 2000.

- India allowed private companies in insurance sector in 2000, setting a limit on FDI to 26%, which was increased to 49% in 2014 and further increased to 74% in the Union Budget (Feb’21).

- The market share of private sector companies in the non-life insurance market rose from 15% in FY04 to 49.3% in FY21.

- Private insurers like HDFC, ICICI and SBI have been some tough competitors for providing life as well as non-life products to the insurance sector in India.

- The IPO of Life Insurance Corporation (LIC) of India was the largest IPO ever in India and the sixth biggest IPO globally of 2022. As of November 2022, listing of LIC accounted for more than a third of resources mobilised in the primary equity market until November 2022.

- Insurance market in India is expected reach US$ 222 billion by 2026.

- Robotic Process Automation (RPA) and AI will occupy center stage in insurance, driven by newer data channels, better data processing capabilities and advancements in AI algorithms.

- Bots will become mainstream in both the front and back-office to automate policy servicing and claims management for faster and more personalized customer service.

- Insurers can now launch new health insurance products without IRDAI’s nod. Earlier the flexibility was given for group insurance products but now retail products have also come under the new norms.

- The insurance industry is expected to use this opportunity for introduction of customized and innovative products, expansion of the choices available to the policyholders in order to address the dynamic needs of the market, which will further help in enhancing the insurance penetration in India.

- Bajaj Allianz Life Insurance, a private life insurer, has entered into a strategic partnership with City Union Bank, one of the oldest private sector banks in India. This partnership will help the private life insurer offer a wide array of life insurance solutions to the bank’s existing and future customers, across their 727 branches.

- In October 2022, Policybazaar's PBPartners launches its mobile app to facilitate the ease of insurance business for its advisors digitize their insurance business.

- Canara HSBC Life Insurance launched its‘Canara HSBC Life Insurance App’ on the 75th Independence Day of India. The app, available on android, iOS devices and web portal, offers access to policy details, the option to receive timely alerts, pay the premium, and track fund value among others.

- ICICI Lombard and Airtel Payments bank have entered into a partnership for providing cyber insurance in February 2022.

- Probus Insurance receives US$ 6.7 million in funding from a Swiss impact fund in December 2021.

- Companies are trying to leverage strategic partnership to offer various services as follows:

- In November 2021, ICICI Lombard collaborated with Vega to provide a personal accident insurance cover with every online Vega helmet purchase to increase road safety awareness among customers.

- In November 2021, ICICI Prudential Life Insurance partnered with NPCI Bharat BillPay, a subsidiary of National Payments Corporation of India (NPCI), to offer ClickPay feature to its customers.

- In November 2021, the Competition Commission of India (CCI) approved HDFC Life Insurance’s acquisition of 100% shareholding in Exide Life Insurance. The move is expected to strengthen HDFC Life’s position in South India.

- In November 2021, Willis Towers Watson acquired the remaining 51% shares in WTW India, taking the company’s holding in WTW India to 100%.

- In November 2021, Acko, a digital insurance start-up, raised US$ 255 million in funds, taking the company’s valuation to ~US$ 1.1 billion.

- In September 2021, ZestMoney raised US$ 50 million to enter new business opportunities in the insurance sector.

- In August 2021, PhonePe announced that it has received preliminary approval from IRDAI to act as a broker for life and general insurance products. As a result, the company can now offer insurance advice to its 300+ million users.

- In FY21, LIC achieved a record first-year premium income of Rs. 56,406 crore (US$ 7.75 billion) under individual assurance business with a 10.11% growth over last year.

- In FY23, non-life insurers (comprising general insurers, standalone health insurers and specialized insurers) recorded a 16.4% growth in gross direct premiums. In India, gross premiums written off by non-life insurers reached US$ 31 billion in FY23 and US$ 17.29 billion in FY24 (until September 2023), from US$ 28.14 billion in FY22, driven by strong growth from general insurance companies.

- In August 2021, ICICI Prudential Life Insurance tied up with the National Payments Corporation of India (NPCI) to provide a unified payments interface autopay.

Government Initiatives

The Government of India has taken number of initiatives to boost the insurance industry. Some of them are as follows:

- The Union Budget 2023-24 has proposed to limit the income tax exemption on the proceeds of high value life insurance policies. Mooted as part of an emphasis on better targeting of tax concessions and exemptions, the proposal means that income from life insurance policies with an aggregate premium up to Rs. 5 lakh (US$ 6,075) will be exempt from taxation.

- The government’s flagship initiative for crop insurance, Pradhan Mantri Fasal Bima Yojana (PMFBY), has led to significant growth in the premium income for crop insurance.

- Ayushman Bharat (Pradhan Mantri Jan Arogya Yojana) (AB PMJAY) aims at providing a health cover of Rs. 5 lakh (US$ 6,075) per family per year for secondary and tertiary care hospitalization.

- Insurance cover for 44.6 crore persons under PM Suraksha Bima and PM Jeevan Jyoti Yojana was provided during FY23.

- In 2022, the Indian government plans to sell a 7% stake in LIC for Rs. 50,000 crore (US$ 6.62 billion). This is the largest initial public offering (IPO) in India.

- In November 2021, the Indian government signed an agreement with the World Bank for a US$ 40 million project to advance the qualities of health services in Meghalaya, including the state’s health insurance programme.

- In September 2021, the Union Cabinet approved an investment of Rs. 6,000 crore (US$ 804.71 million) into entities, offering export insurance cover to facilitate additional exports worth Rs. 5.6 lakh crore (US$ 75.11 billion) over the next five years.

- In August 2021, the Parliament passed the General Insurance Business (Nationalisation) Amendment Bill. The bill aims to allow privatisation of state-run general insurance companies.

- Union Budget 2021 increased FDI limit in insurance from 49% to 74%. India's Insurance Regulatory and Development Authority (IRDAI) has announced the issuance, through Digilocker, of digital insurance policies by insurance firms.

- Under the Union Budget 2021, Finance Minister Ms. Nirmala Sitharaman announced that the initial public offering (IPO) of LIC will be implemented in FY22, as part of the consolidation in the banking and insurance sector. Though no formal market valuation has been undertaken, LIC’s IPO has the potential to raise Rs. 1 lakh crore (US$ 13.62 billion).

- In June 2021, the government extended a Rs. 50 lakh (US$ 66.85 thousand) insurance coverage scheme for healthcare workers across India until the next one year.

- In February 2021, the Finance Ministry announced to infuse Rs. 3,000 crore (US$ 413.13 million) into state-owned general insurance companies to improve the overall financial health of companies.

- Under Union Budget 2021, fund of Rs. 16,000 crore (US$ 2.20 billion) has been allocated for crop insurance scheme.

Road Ahead

The future looks promising for the life insurance industry with several changes in the regulatory framework which will lead to further changes in the way the industry conducts its business and engages with its customers. Life insurance industry in the country is expected to increase by 14-15% annually for the next three to five years. The scope of IoT in Indian insurance market continues to go beyond telematics and customer risk assessment. Currently, there are 110+ InsurTech start-ups operating in India. These startups are expected to provide a major boost to the industry and help increase India’s insurance penetration which plays a crucial role in the overall development of the country. In the past, the Indian government has played a crucial role in increasing the scope of the insurance sector through various policies and schemes. This trend will continue in the further through schemes like the Pradhan Mantri Fasal Bima Yojana (PMFBY) providing crop insurance and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) providing life insurance coverage to the youth at an affordable price. Schemes like these coupled with India’s demographic factors such as a growing middle class, young insurable population and growing awareness of the need for protection and retirement planning will support the growth of the Indian insurance sector.

Note: Conversion rate used for November 2023 is Rs. 1 = US$ 0.012,

*- New Business Premium Value is until November 2023, Renewable Premium Value in India is until March 2022 (FY21)

References: Media Reports, Press Releases, Press Information Bureau, Union Budget 2021-22, Insurance Regulatory and Development Authority of India (IRDA), Crisil, Union Budget 2023-24, Economic Survey 2022-23

Related News

MORE

IBEF Campaigns

MORE

India Organic Biofach 2022

Ibef Organic Indian Pavilion BIOFACH2022 July 26th-29th, 2022 | Nuremberg, ...

Case Studies

MOREPromoting Indigenous Start-ups: Case Study of Investor Interest in Small-town Start-ups

As urban markets become saturated, investors are turning their gaze towards the untapped potential of small-town innovation, driven by a desire to fos...

India's White Revolution

The "White Revolution" in India refers to the successful implementation of Operation Flood, a dairy development program launched on January ...

The Growth of Ayurveda in India

Ayurveda, an ancient health system originating from India, has a longstanding history. It revolves around using plants and herbs to maintain health an...

IBEF BLOG

MORE

India's Solar Power Revolution

India is leading the renewable energy revolution, with a strategic emphasis...

Empowering MSMEs: Fintech Solutions for Small Businesses in India

Micro, small, and medium enterprises (MSMEs) are the backbone of the Indian...

Unlocking India's Digital SME Credit Gap and Economic Potential

The Indian economy thrives on the contributions of the Micro, Small, and Me...

Partners