Introduction

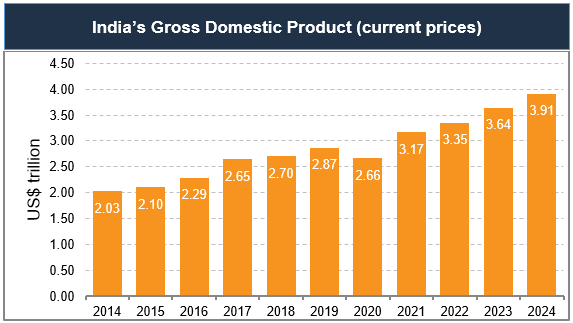

India’s economic momentum remains strong, underpinned by resilient domestic demand and sustained macroeconomic stability. In FY 2025–26, Real GDP (GDP at Constant Prices) is estimated to reach Rs. 3,22,58,000 crore, rising from Rs. 2,99,89,000 crore in FY 2024–25, reflecting a robust growth of 7.6%. At current prices, Nominal GDP is projected to reach Rs. 3,45,47,000 crore (US$ 3.91 trillion) in FY 2025–26, from Rs. 3,18,07,000 crore (US$ 3.60 trillion) in the previous year, registering a growth of 8.6%. On the production side, Real Gross Value Added (GVA) is estimated at Rs. 2,94,40,000 crore, up from Rs. 2,73,36,000 crore in FY 2024–25, indicating a growth of 7.7%, while Nominal GVA is expected to expand to Rs. 3,13,61,000 crore (US$ 3.55 trillion) from Rs. 2,88,54,000 crore (US$ 3.26 trillion), marking a growth of 8.7%. In Q3 FY26, Real GDP is estimated at Rs. 84,54,000 crores against Rs. 78,41,000 crores in Q3 FY25, while Nominal GDP rose to Rs. 90,91,000 crores from Rs. 83,46,000 crores, showing continued quarterly momentum. Collectively, these trends highlight India’s position as one of the fastest-growing major economies, supported by broad-based expansion across sectors.

Market Overview

India is home to 126 unicorns, with six new startups achieving unicorn status in 2025.

India’s current account deficit widened in Q3 FY 2025–26 (October–December), primarily due to a higher merchandise trade deficit.

The deficit stood at Rs. 1.18 lakh crore (US$ 13.2 billion), compared with Rs. 0.95 lakh crore (US$ 11.3 billion) in the same quarter last year.

The merchandise trade deficit increased to Rs. 8.34 lakh crore (US$ 93.6 billion) from Rs. 6.70 lakh crore (US$ 79.3 billion) in Q3 FY25, while the services surplus improved to Rs. 5.12 lakh crore (US$ 57.5 billion) from Rs. 4.32 lakh crore (US$ 51.2 billion) during the same period.

Source: World Bank

Recent Developments

India is primarily a domestic demand-driven economy, with consumption and investments contributing to 70% of the economic activity. With India’s economy showing resilient growth, supported by strong domestic demand, policy reforms, and a healthy investment pipeline, several new projects and developments are underway across key sectors. According to World Bank, India must continue to prioritise lowering inequality while also putting growth-oriented policies into place to boost the economy. In view of this, there have been some developments that have taken place in the recent past. Some of them are mentioned below.

- On the FDI front, according to the Department for Promotion of Industry and Internal Trade (DPIIT), India's cumulative FDI inflow stood at US$ 1.14 trillion between April 2000-December 2025; with major share of FDI equity inflow, coming from Singapore at Rs. 13,72,320 crore (US$ 192.53 billion) with a total share of 25%, followed by Mauritius at Rs. 11,34,884 crore (US$ 185.02 billion) with 24%, the USA at Rs. 5,60,990 crore (US$ 78.45 billion) with 10%, the Netherlands at Rs. 3,82,995 crore (US$ 55.60 billion) with 7%, and Japan at Rs. 3,11,507 crore (US$ 47.59 billion) with 6%.

- As of March 27, 2026, India’s foreign exchange reserves stood at Rs. 65,20,745 crore (US$ 688.05 billion).

- In Q1 CY2026 (January–March), India recorded 316 Private Equity (PE)–Venture Capital (VC) deals valued at Rs. 82,660 crore (US$ 9.1 billion), reflecting continued investor participation despite global geopolitical uncertainties and temporary supply chain disruptions linked to the ongoing West Asia conflict. In Q1 CY2025, PE-VC investments stood at Rs. 1,01,320 crore (US$ 11.7 billion), highlighting the strong base of investment activity in the previous year. In March 2026 alone, investments were valued at Rs. 35,310 crore (US$ 3.8 billion), compared with Rs. 40,660 crore (US$ 4.7 billion) in March 2025.

- During FY 2025–26, Foreign Portfolio Investor (FPI) activity in India reflected portfolio rebalancing and selective capital allocation across asset classes amid evolving global market conditions. While investors adopted a calibrated approach towards equity markets, debt instruments continued to attract strong inflows of Rs. 25,807 crore (US$ 2.92 billion), supported by stable macroeconomic fundamentals, policy continuity and India’s improving bond market attractiveness. FPIs also channelled Rs. 2,699 crore (US$ 0.31 billion) into mutual fund schemes, indicating sustained preference for diversified and professionally managed market exposure. Alternative Investment Funds (AIFs) also recorded inflows, while cumulative FPI investments in India stood at Rs. 14,84,403 crore (US$ 168.00 billion) by the end of FY 2025–26, underlining long-term foreign investor confidence in India’s growth story. Domestic Institutional Investors (DIIs) continued to play a stabilising role in the equity cash market during FY 2025–26 (April–December 2025), recording net purchases of around Rs. 5.99 lakh crore (US$ 66.55 billion), with strong participation from mutual funds, insurance companies and pension funds supporting market resilience.

- India’s manufacturing sector remained in expansionary territory in March 2026, with the seasonally adjusted HSBC India Manufacturing Purchasing Managers’ Index (PMI) at 53.9, following a strong 56.9 in February 2026. The index continued to stay above the neutral 50-mark, reflecting sustained growth in overall business conditions and healthy momentum across the manufacturing sector. New orders and output continued to rise, supported by steady domestic demand and inventory building, while firms also increased employment and input purchases to strengthen contingency stocks.

- India’s consumer price inflation remained well-anchored in March 2026, reflecting a stable price environment across the economy. Headline inflation, based on the All-India Consumer Price Index (CPI), stood at 3.40% year-on-year, compared with 3.21% in February 2026, indicating manageable price pressures across both rural and urban regions. Rural inflation was recorded at 3.63%, while urban inflation stood at 3.11% during the month.

- India’s GST collections continued to demonstrate strong revenue resilience, supported by steady economic activity and improved compliance levels. Total Net GST revenue in March 2026 stood at Rs. 1.78 lakh crore (US$ 20.14 billion), registering a year-on-year growth of 8.2% compared with Rs. 1.64 lakh crore (US$ 18.49 billion) in March 2025. On a cumulative basis, yearly net GST collections reached Rs. 19.35 lakh crore (US$ 219.03 billion) in FY 2025–26, reflecting a year-on-year growth of 7.1% over Rs. 18.07 lakh crore (US$ 204.46 billion) in FY 2024–25.

- India’s aviation sector continued to witness steady growth in passenger traffic during FY 2025–26 (April–March). Total passengers handled stood at 420.09 million, compared with 412.09 million in FY 2024–25, registering a growth of 1.9%.

- The government is focusing on renewable energy sources and has achieved a major clean energy milestone by generating 50% of its power from renewable sources, five years ahead of its 2030 target. India is committed to achieving its Net Zero Emissions ambition by 2070 through a five-pronged strategy, ‘Panchamrit’. Moreover, India ranked 3rd in the renewable energy country attractiveness index.

- India secured 38th position out of 139 economies in the Global Innovation Index 2025. India rose from 81st position in 2015 to 38th position in 2024. India ranks in 3rd position in the global number of scientific publications.

- India’s industrial activity continued to witness steady expansion in March 2026, with the Index of Industrial Production (IIP) growing by 4.1% year-on-year, supported by sustained momentum across key sectors. The manufacturing sector recorded a 4.3% increase, while mining expanded by 5.5%, reflecting strength in core industrial segments. Electricity generation also remained positive at 0.8%, contributing to overall industrial performance. The IIP index rose to 173.2 in March 2026, up from 166.3 in March 2025, indicating continued expansion in India’s industrial base. Within manufacturing, 14 out of 23 industry groups recorded growth, with key contributors including basic metals, motor vehicles and machinery & equipment, highlighting broad-based industrial activity.

- The government has set a calibrated wheat procurement target of 343.35 lakh metric tonnes (LMT) for the 2026–27 rabi marketing season, ensuring efficient stock management and smooth market operations. As per the latest data, total wheat procurement has reached 31.87 lakh metric tonnes (LMT) as of end-April 2026, reflecting the ongoing progress of procurement across key producing states.

Government Initiatives

Over the years, the Indian government has introduced many initiatives to strengthen the nation's economy. The Indian government has been effective in developing policies and programmes that are not only beneficial for citizens to improve their financial stability but also for the overall growth of the economy. Over recent decades, India's rapid economic growth has led to a substantial increase in its demand for exports. Besides this, a number of the government's flagship programmes, including Make in India, Start-up India, Digital India, the Smart City Mission, and the Atal Mission for Rejuvenation and Urban Transformation, are aimed at creating immense opportunities in India. In this regard, some of the initiatives taken by the government to improve the economic condition of the country are mentioned below:

- On March 17, 2026, the Union Cabinet approved the ‘Mission for Aatmanirbharta in Pulses’ with an outlay of Rs. 11,440 crores (US$ ~1.27 billion) to achieve self-sufficiency in pulses by 2030–31.

- On February 28, 2026, Prime Minister Narendra Modi inaugurated Micron Technology’s Semiconductor Assembly, Test and Packaging (ATMP) facility in Sanand, Gujarat, marking the commencement of commercial production.

- On February 20, 2026, the Government of Gujarat signed an MoU with Larsen & Toubro VYOMA to develop a 250 MW green AI-ready data centre campus at Dholera SIR with an investment of Rs. 25,000 crores (US$ ~3 billion).

- On January 2, 2026, the Government launched two key interventions under the Export Promotion Mission to strengthen MSME exports, including a 2.75% interest subvention on pre- and post-shipment credit and collateral guarantee support of up to 85% through CGTMSE.

- Under the Startup India initiative, the Government continues to strengthen the start-up ecosystem through targeted funding, seed support, and credit guarantees. As of October 2025, women-led start-ups received investments and financial support of over Rs. 3,157 crore (US$ 0.38 billion) through the Fund of Funds for Startups, Startup India Seed Fund Scheme, and Credit Guarantee Scheme, reinforcing inclusive entrepreneurship and early-stage innovation across sectors.

- The Ministry of Labour & Employment signed an MoU with Zomato on October 14, 2025, to enhance employment opportunities through the National Career Service (NCS) portal. Under the agreement, Zomato will list around 2.5 lakh job opportunities annually, supporting the growth of the gig economy and promoting formal, technology-enabled livelihoods across India.

- The Production Linked Incentive (PLI) programme has continued to strengthen India’s manufacturing base and enhance domestic value addition across priority sectors. As of December 2025, realised investments under PLI schemes reached Rs. 2,16,000 crore (US$ 24.44 billion), leading to incremental production and sales of Rs. 20,41,000 crore (US$ 230.93 billion) and generating over 14.39 lakh jobs (direct and indirect).

- In August 2025, Prime Minister Mr. Narendra Modi launched two major agriculture schemes worth Rs. 35,440 crore (US$ 4 billion), the PM Dhan-Dhaanya Krishi Yojana and the Mission for Aatmanirbharta in Pulses, aimed at boosting self-reliance, productivity, and farmers’ income. He also inaugurated and laid foundation stones for projects worth over Rs. 6,200 crore (US$ 709 million) across agriculture, animal husbandry, fisheries, and food processing sectors.

- On July 5, 2025, the Union Cabinet approved the Rs. 1,00,000 crore (US$ 11.72 billion) Research, Development and Innovation (RDI) Scheme, launching long‑term, low‑ or zero‑interest funding via a special purpose fund under the ANRF to jump‑start India’s R&D ecosystem and support deep‑tech and startup innovation.

- In March 2025, the Government announced several measures to boost industrial growth and investments, including initiatives such as Make in India, Start-up India, PM GatiShakti, and Production Linked Incentive (PLI) Schemes. The Cabinet Committee on Economic Affairs also approved 12 new projects worth Rs. 28,602 crore (US$ 325.02 million) under the National Industrial Corridor Development Programme (NICDP), spanning 10 states, to strengthen India’s manufacturing base and attract investments.

Road Ahead

India’s economic outlook remains robust, supported by strong macroeconomic fundamentals, resilient domestic demand and sustained investment momentum. The economy continues to rank among the fastest-growing major economies globally, driven by broad-based expansion across manufacturing, services and infrastructure, alongside steady improvement in industrial and business activity.

A stable external position, supported by a manageable current account balance and consistent capital flows, reinforces confidence in India’s long-term growth trajectory. Despite evolving global uncertainties, investor interest remains intact across key sectors, backed by policy stability and structural growth drivers.

Domestic demand continues to act as a key anchor, supported by stable inflation, rising mobility and travel activity, healthy tax collections and strong participation from domestic institutional investors.

Ongoing government initiatives to boost manufacturing, innovation, renewable energy and food security are further strengthening the foundation for sustained growth.

Partners