Advantage India

Growing

Demand

*Indian food processing market size reached US$ 354.5 billion in FY24 and is expected to reach US$ 535 billion by FY26.

*The milk production has increased from 230.58 million tonnes in 2022-23 to 239.30 million tonnes in 2023-24, registering a growth of 3.78% over the previous year.

*Indian dairy firms are projected to grow 11-13% in FY26, led by value-added products, with improved margins and Rs. 3,400 crore (US$ 398 million) capex.

*India’s Rs. 46,571 crore (US$ 5.29 billion) snack market is seeing startup challenges to legacy brands and is set to reach Rs. 1,01,811 crore (US$ 11.57 billion) by 2033, with namkeen adding Rs. 39,591 crore (US$ 4.5 billion) by 2029.

Attractive

Opportunities

*Increased rural consumption presents an opportunity for expanding distribution networks in tier-2 and tier-3 cities.

*The quick commerce market in India currently exhibits a penetration rate of only 7% of the potential market, with a total addressable market of US$ 45 billion, surpassing that of food delivery, indicating that a significant opportunity remains untapped.

*India’s healthy snack market was valued at US$ 3.13 billion in 2025, and it is expected to reach US$ 4.77 billion by 2034, exhibiting a CAGR of 4.80%, driven by functional, natural options, quick commerce, and premiumisation.

*FMCG giants are gearing up to capitalise on the heating Indian pet food market, driven by the rise in pet ownership and disposable income of owners.

Policy

Support

*The Union Budget 2025-26 provides a strong push to consumer spending, particularly benefiting the FMCG industry. The increase in disposable income, rural development focus, and MSME support create an ideal environment for growth.

*MoFPI has approved over 1.44 lakh food processing projects through its flagship schemes to boost rural economies, strengthen supply chains, and promote Indian brands globally.

Higher

Investments

*ITC Ltd. plans Rs. 20,000 crore (US$ 2.33 billion) investment over the next five to six years, focusing on FMCG growth, margin expansion, new product launches, horticulture, and AI-driven operations.

*Hindustan Unilever plans to invest Rs. 2,000 crore over two years to expand manufacturing in premium beauty, wellbeing, and home care segments, capitalizing on rising premiumization demand in India’s FMCG market.

*Nestlé India reported a 46% YoY increase in Q3 FY26 profit to US$ 115.19 million (Rs. 1,018 crore), driven by tax cuts boosting consumer demand. Revenue rose ~19% with strong volume growth across packaged foods, supported by product launches, rural expansion, and quick-commerce channels.

Introduction

The FMCG sector in India has expanded steadily, supported by consumer-driven growth and higher product prices, particularly for essential goods. It provides employment to around three million people, accounting for approximately 5% of total factory employment in the country. As India’s fourth-largest sector, FMCG plays a vital role in the economy, with household and personal care products alone contributing 50% of total FMCG sales.

The industry is projected to maintain healthy momentum, supported by rising disposable incomes, a young consumer base, increasing brand awareness, and favourable government initiatives and policies. Household FMCG spending in India rose 8% to Rs. 17,792 crore (US$ 2.07 billion) by April 2025 and is expected to increase further to around Rs. 20,000 crore (US$ 2.27 billion) by the end of 2025, driven by higher consumption across staples as well as non-staples. More importantly, India’s vast middle-class population, which is larger than the total population of the USA, and its median age of just 27 are shaping consumption trends. Rising aspirations, greater financial inclusion, and social safety nets are further fuelling demand.

The sector continues to demonstrate resilience, with companies focusing on efficient manufacturing, supply chain management, consumer insights, and digital-first communication strategies to withstand disruptions and create long-term value. According to NielsenIQ, India’s FMCG market grew 13.9% in value and 6% in volume in Q1 FY26, led by rural demand, smaller pack sizes, and e-commerce growth. Key companies also posted steady performance in the same quarter. Dabur expected single-digit revenue growth, Nykaa’s beauty segment registered mid-20% GMV growth, Tata Group’s Trent expanded 20%, and Kalyan Jewellers rose 31%, supported by improving urban sentiment and easing inflation.

As per NielsenIQ, India’s FMCG sector posted steady momentum in the Q2 FY26 with value growth of 12.9% and a 5.4% rise in volumes, supported by stronger rural demand with 7.7% volume expansion. India’s FMCG sector witnessed a clear demand shift in 2025, with overall volume growth moderating to 4.1% (down from 4.7% in 2024), primarily due to a sharp rural slowdown, where growth declined to 3.6% from 5%, while urban markets showed relative resilience with a marginal uptick to 4.6% from 4.5%, indicating a structural rebalancing of consumption trends and highlighting urban recovery as a key stabilizing force amid weakening rural momentum. Diwali boosted FMCG sales, with essentials, dairy, oils, and snacks seeing strong demand and e‑commerce orders rising over 85% in the first week festive season sale.

India’s direct selling industry is also expanding, with sales of Rs. 22,142 crore (US$ 2.58 billion) in FY24, reflecting 4.4% YoY growth. Over the last five years, the sector has clocked a 7.15% CAGR, with the number of active direct sellers reaching 88 lakh. Female participation has also risen from 37% in FY23 to 44% in FY24, highlighting the growing inclusivity of this channel.

Looking ahead, India’s FMCG sector is expected to record a slight revenue increase of 100 to 200 basis points, bringing growth to 6 to 8% in FY26, supported by stable rural demand and a revival in urban markets. The urban segment currently contributes about 62% of total revenue, but rural India has emerged as a stronger growth driver in recent years. Semi-urban and rural regions now account for 50% of total rural spending on FMCG, with rising incomes and evolving consumer preferences narrowing the urban–rural gap.

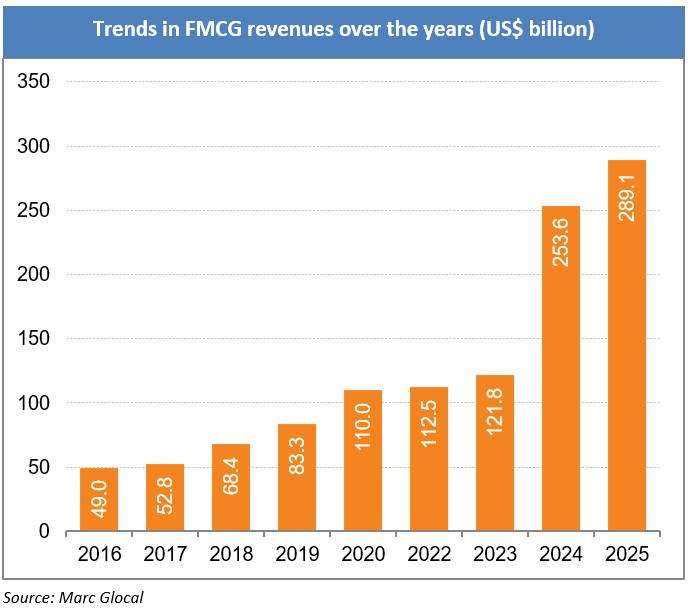

Market Size

The Indian FMCG market generated revenue of Rs. 25 lakh crore (US$ 289.1 billion) in 2025 and is expected to grow at a CAGR of 17.3% through 2025–30, reaching nearly US$ 642.87 billion by 2030. In 2025, the urban segment contributed 62% while rural India accounted for more than 38% of annual FMCG sales, highlighting the importance of both markets in driving growth.

FMCG household consumption across Indian cities exhibited a clear shift toward metro-driven concentration rather than uniform city-wise distribution, with e-commerce accounting for approximately 14% of FMCG sales across metros and increasing further to nearly 18% in the top 8 cities, significantly higher than the ~6% urban average. Notably, southern metro clusters emerged as the most digitally advanced consumption hubs, crossing ~21% e-commerce penetration, underscoring a strong shift toward online-led household purchasing behaviour in select urban pockets, even as overall urban FMCG growth remained relatively moderate in the range of ~2.3% to 4.6%, reflecting a structurally uneven but increasingly digital-first consumption landscape across India’s cities.

Leading FMCG players are leveraging rural India’s potential. ITC expanded rural FMCG reach via strong distribution networks, Dabur strengthened rural presence through affordable packs, and Zydus Wellness focused on rural health demand, as rural FMCG growth (~3.6%) remained a key driver versus urban (~4.6%),

supporting overall FY26 consumption stability. Dabur derives 45–50% of its revenue from rural markets, reaching over 1,31,000 villages and 1.42 million outlets. Hindustan Unilever generates 35–40% of its revenue from rural areas, supported by its Shikhar app, which has 1.4 million retailers on board and a 70% monthly active user rate.

Emerging categories are also boosting the FMCG landscape. India’s pet economy is projected to grow from Rs. 89,743.5 crore (US$ 10.5 billion) in FY24 to Rs. 1,38,461.4 crore (US$ 16.2 billion) by FY32 at a CAGR of 5.65%. India’s healthy snack market was valued at US$ 3.13 billion in 2025, and it is expected to reach US$ 4.77 billion by 2034, exhibiting a CAGR of 4.80%, driven by functional, natural options, quick commerce, and premiumisation. The milk production has increased from 230.58 million tonnes in 2022-23 to 239.30 million tonnes in 2023-24, registering a growth of 3.78% over the previous year. The dairy industry is projected to expand by 13–14% in FY25, backed by strong demand and increased milk supply. Meanwhile, the alcoholic beverage (alcobev) industry is set to grow 8–10% in FY26, reaching Rs. 5,30,000 crore (US$ 61.97 billion). India’s Rs. 46,571 crore (US$ 5.29 billion) snack market is seeing startup challenges to legacy brands and is set to reach Rs. 1,01,811 crore (US$ 11.57 billion) by 2033, with namkeen adding Rs. 39,591 crore (US$ 4.5 billion) by 2029.

The quick commerce market in India currently exhibits a penetration rate of only 7% of the potential market, with a total addressable market of US$ 45 billion, surpassing that of food delivery, indicating that a significant opportunity remains untapped. It now accounts for 70–75% of total e-grocery orders, compared to 35% in 2022, and is expanding at a CAGR of 70–80%. Operating across 80 cities, India is the first market globally to scale quick commerce, which has delivered FMCG companies a 50–100% sales increase in FY25.

Government initiatives and policies continue to support growth. India’s PLI schemes, with Rs. 1.91 lakh crore (US$ 21.70 billion) total outlay have driven over Rs. 2.16 lakh crore (US$ 24.55 billion) investments and significant production growth, strengthening manufacturing, including food processing and FMCG supply chains. In Union Budget 2026, the government continued strengthening PLI schemes, proposing Rs. 40,000 crore (US$ 4.55 billion) allocation for electronics and considering expansion into emerging sectors like AI and advanced manufacturing. Also, the Union Government approved a Production Linked Incentive (PLI) scheme for the food processing sector with a budget outlay of Rs. 10,900 crore (US$ 1.46 billion). Till June 2025, the scheme had approved 278 units of 170 applicants, attracted Rs. 9,032 crore (US$ 1.04 billion) in investments, created 3.4 lakh jobs, and added 35 lakh MT of annual capacity. The Ministry of Food Processing Industries (MoFPI) has also sanctioned over 1.44 lakh projects through its flagship schemes to boost rural economies, strengthen supply chains, and promote Indian food brands globally.

Digital transformation is reshaping consumption. India has 1,002.85 million internet subscribers as of April–June 2025, with rural penetration at 46 per 100 people, creating opportunities for satellite internet, digital inclusion, and e-commerce growth. E-commerce accounted for 17% of FMCG consumption among affluent buyers in 2024, with average spends of Rs. 5,620. India’s e-commerce industry, valued at Rs. 10,82,875 crore (US$ 125 billion) in FY24, is expected to grow to Rs. 29,88,735 crore (US$ 345 billion) by FY30 at a 18.4% CAGR. The online grocery segment alone is projected to expand from US$ 4.54 billion in 2022 to US$ 76.76 billion by 2032, growing at a CAGR of 32.7%. Digital payments, which reached US$ 300 billion in 2021, are projected to touch US$ 1 trillion by 2026.

The D2C market crossed Rs. 6,96,400 crore (US$ 80 billion) in 2024 and is expected to exceed Rs. 8,70,500 crore (US$ 100 billion) in 2025. FMCG new product launches rose 1.8 times in the year ending May 2025, though only 4% reached 1% market penetration due to intense competition from regional and D2C brands. Legacy companies are adapting: Marico entered a strategic deal with PVR INOX to acquire its 4700BC premium snacks brand for Rs. 226.8 crore (US$ 25.77 million), expanding its FMCG portfolio and strengthening presence in packaged snacking.

Around two‑thirds of acquisitions by FMCG firms from FY21 to FY25 have been in the direct‑to‑consumer (D2C) space, per Crisil Ratings.

Competition is intensifying between global majors, domestic giants, and start-ups. FMCG leaders such as Johnson & Johnson, Himalaya, HUL, ITC, and Lakmé are facing challenges from digital-first players like Mamaearth, Sugar, The Moms Co., and Nua, which reached Rs. 100 crore revenue milestones far faster than traditional brands. Global majors are also scaling up: ITC announced a capital expenditure plan of around Rs. 20,000 crore (US$ 2.39 billion) across FMCG and other businesses, focusing on technology, expansion, and capacity building to strengthen long-term growth and market presence. Hindustan Unilever announced an investment of up to Rs. 20,000 crore (US$ 2.39 billion) to expand manufacturing capacity in premium segments, focusing on beauty and personal care to drive growth and improve margins.

India’s FMCG sector remained the largest advertiser in 2024, contributing around 34% of total ad expenditure, with spends estimated at Rs. 31,428 crore (US$ 3.57 billion), maintaining its dominant share in the advertising market. With rising incomes, shifting consumer preferences, growing digital penetration, and robust policy support, the sector is well positioned to remain one of the strongest drivers of India’s consumption-led growth story.

Investments

- From April 2000 to December 2025, India’s food processing industry has received cumulative FDI inflows of approximately Rs. 1,10,459.97 crore (US$ 15.86 billion), reflecting steady growth in foreign investment in the sector.

- In February 2026, Hindustan Unilever plans to invest Rs. 2,000 crore (US$ 227.27 million) over two years to expand manufacturing in premium beauty, wellbeing, and home care segments, enhancing supply chain agility, leveraging automation, and capitalizing on rising premiumization demand in India’s FMCG market.

- In January 2026, Nestlé India reported a 46% YoY increase in Q3 FY26 profit to US$ 115.19 million (Rs. 1,018 crore), driven by tax cuts boosting consumer demand. Revenue rose ~19% with strong volume growth across packaged foods, supported by product launches, rural expansion, and quick-commerce channels.

- In January 2026, Marico entered a strategic deal with PVR INOX to acquire its 4700BC premium snacks brand for Rs. 226.8 crore (US$ 25.77 million), expanding its FMCG portfolio and strengthening its presence in packaged snacking.

- In January 2026, Dharampal Satyapal Group ended its collaboration with Swiss chocolate brand Läderach in India, marking a strategic shift in its premium confectionery segment and redefining its partnership-led growth approach.

- In December 2025, Reliance Consumer acquired a majority stake in Udhaiyams Agro Foods (FMCG staples & snacks expansion), strengthening Reliance’s packaged foods and FMCG distribution portfolio.

- In December 2025, HUL reinforced its premium FMCG investment strategy in beauty & personal care segments, focusing on high-growth categories to offset slow volume growth in mass products.

- In November 2025, Reliance Consumer Products Ltd (RCPL) entered India’s pet care market with the launch of Waggies, offering science-backed, affordable nutrition for pets.

- In November 2025, PepsiCo India launched Red Rock Deli, a gourmet chips brand, and L’Oréal introduced La Roche-Posay skincare products in India to expand their global offerings.

- In September 2025, Amazon expanded its quick commerce service, Amazon Now, to Mumbai, offering groceries, essentials, and over 40,000 FMCG items with rapid delivery.

- In August 2025, Reliance Industries announced plans to invest Rs. 40,000 crore (US$ 4.7 billion) over the next three years to build Asia’s largest integrated food parks with AI-driven automation, robotics, and sustainable technologies.

- ITC Ltd. plans Rs. 20,000 crore (US$ 2.33 billion) investment over the next five to six years, focusing on FMCG growth, margin expansion, new product launches, horticulture, and AI-driven operations.

- Reliance Consumer Products Limited plans to invest Rs. 8,000 crore (US$ 929.3 million) over the next 12-15 months from September 2025 to expand its beverage manufacturing capacity across 10-12 new plants nationwide.

- In September 2025, Adani Wilmar acquired G.D. Foods (Tops ketchup brand) in a Rs. 603 crore (US$ 70 million) deal in stages, 80 % upfront and remaining 20 % over three years, to expand its value-added food portfolio, adding eight new categories including sauces, jams, pickles and instant mixes.

- In August 2025, Reliance Consumer Products Limited (RCPL) acquired a majority stake in Naturedge Beverages (Shunya herbal-functional drinks), marking its entry into the fast-growing herbal and functional beverages segment.

- In July 2025, Chaudhary Group and Bikaji Foods form a 50:50 joint venture to launch Indian snacks in Nepal, setting up local production and creating thousands of jobs in the FMCG market.

- In May 2025, Rasna acquired the Jumpin ready-to-drink beverage brand from Hershey’s India, valued at approximately Rs. 350 crore (US$ 40.32 million), positioning itself to target Rs. 1,000 crore (US$ 116.2 million) in revenue over the next two years.

- In April 2025, ITC Limited acquired 100% of Sresta Natural Bioproducts (maker of 24 Mantra Organic) in a Rs. 472.5 crore (US$ 54.9 million) deal to strengthen its organic food portfolio.

- PepsiCo and Tata Consumer Products partner to launch fusion snacks combining Kurkure and Ching's Secret, targeting India’s ethnic snacks market with more than 20% annual growth.

- In 2025, ITC and Prataap Snacks launched Korean chips, Pringles introduced fusion and desi masala variants, Unibic rolled out Snappers, and Marico’s Saffola added a Munchies range.

- In 2025, Horlicks from Hindustan Unilever launched the Plus range for women, mothers, and men.

- Reliance Consumer, which relaunched Campa in 2023, expanded in 2025 with 15–20 variants spanning cola, nectar, energy, and sports drinks, including regional flavours.

- In summer 2025, AI drove 50% of new FMCG launches in India, influenced pricing in 60% of markets, boosted cold beverages and packaged foods by 80%, quick commerce presence by 30%, and Kombucha listings by 150% without discounts.

- In 2024, Marico launched the Kaya Youth oxy-infusion range with an AI-based analyser to measure skin oxygen levels and recommend personalised routines.

- In August 2024, Emami Limited acquired full ownership of The Man Company for Rs. 177.63 crore (US$ 21 million).

- In July 2024, Chairman and Managing Director Mr. Sanjiv Puri said ITC Ltd. has come up with a Rs. 20,000 crore (US$ 241.55 million) capex plan for the mid-term to expand its capacities in fast moving consumer goods (FMCG), paperboard and other businesses.

- In February 2024, Varun Beverages announced of investing Rs. 3,500 crores (US$ 421.69 million) to setup manufacturing plants, while generating 1,500 employment opportunities.

Government Initiatives

Some of the major initiatives taken by the Government to promote the FMCG sector in India are as follows:

- India’s PLI schemes, with Rs. 1.91 lakh crore (US$ 21.70 billion) total outlay have driven over Rs. 2.16 lakh crore (US$ 24.55 billion) investments and significant production growth, strengthening manufacturing, including food processing and FMCG supply chains.

- In Union Budget 2026, the government continued strengthening PLI schemes, proposing Rs. 40,000 crore (US$ 4.55 billion) allocation for electronics and considering expansion into emerging sectors like AI and advanced manufacturing.

- The Union government approved a new PLI scheme for the food processing sector, with a budget outlay of Rs. 109 billion (US$ 1.46 billion). Incentives under the scheme will be disbursed for six years to 2026-27.

- The government's initiative to promote millets for its health benefits would increase the consumption and production of the millets in the nation. To support this, the government declared that the Indian Institute of Millet Research in Hyderabad will become a worldwide centre of excellence for the exchange of best practices, knowledge, and innovations.

- The PLI Scheme for Food Processing Industries (PLISFPI), with a budget of Rs. 10,900 crore (US$ 1.3 billion) for 2021-27, has approved 278 units of 170 applicants, creating 3.4 lakh jobs, adding 35 lakh MT annual capacity, and disbursing Rs. 1,727 crore (US$ 200.6 million) in incentives till June 2025.

- The scheme has attracted Rs. 9,032 crore (US$ 1.04 billion) in investments, generated Rs. 3,80,000 crore (US$ 43.95 billion) in sales till March 2025, and significantly boosted local raw material procurement, supporting farmer incomes.

- It also promotes Indian food brands globally by reimbursing up to 50% of overseas branding and marketing costs, strengthening their international presence.

- To boost the food processing sector, the Centre has permitted under the Income Tax Act a deduction of 100% of profit for five years and 25% of profit in the next five years in case of new agro-processing industries set up to package and preserve fruits and vegetables.

- Excise Duty of 16% on dairy machinery has been fully waived off and excise duty on meat, poultry and fish products has been reduced from 16% to 8%.

- An amount of Rs. 1,000 crore (US$ 120.7 million) is being set up initially in NITI Aayog for SETU for setting up of incubation centres and enhance skill development to facilitate the startup ecosystem in the country while improving the ease of doing business.

- The governments’ incentives and the FDI funds have helped the FMCG sector strengthen employment, establish a more robust supply chain, and capture high visibility for FMCG brands across established retail markets.

- Union Budget 2023-24 has allocated US$ 976 million for PLI schemes that aims to reduce import costs, improve the cost competitiveness of domestically produced goods, increase domestic capacity, and promote exports.

- The government’s production-linked incentive (PLI) scheme gives companies a major opportunity to boost exports with an outlay of US$ 1.42 billion.

- GST is expected to transform logistics in the FMCG sector into a modern and efficient model as all major corporations are remodelling their operations into larger logistics and warehousing.

Road Ahead

India’s FMCG landscape by 2030 is set for a structural transformation, driven by scale and digital acceleration, with the population expected to exceed 1.5 billion, e-commerce potentially capturing ~40% of FMCG sales, while rural India emerges as a premium growth engine contributing 51% of affordable premium volumes (vs. 45% in 2021)—alongside a strong shift toward health (70% roasted/vacuum-cooked vs. 30% fried foods), sustainability mandates, and hyper-personalised, data-led consumption models.

Rural consumption has increased, led by a combination of increasing income and higher aspiration levels. There is an increased demand for branded products in rural India. On the other hand, with the share of the unorganised market in the FMCG sector falling, the organised sector growth is expected to rise with an increased level of brand consciousness, augmented by the growth in modern retail. Another major factor propelling the demand for food services in India is the growing youth population, primarily in urban regions. India has a large base of young consumers who form most of the workforce, and due to time constraints, barely get time for cooking. Online portals are expected to play a key role for companies trying to enter the hinterlands.

The Internet has contributed in a big way, facilitating a cheaper and more convenient mode to increase a company’s reach. It is estimated that 40% of all FMCG consumption in India will be made online by 2030. E-commerce share of total FMCG sales is expected to increase by 11% by 2030. It is estimated that India will gain US$ 15 billion a year by implementing GST. GST and demonetisation are expected to drive demand, both in the rural and urban areas and economic growth in a structured manner in the long term and improved the performance of companies within the sector.

References: Media Reports, Press Information Bureau (PIB), Union Budget 2023-24, 25-26, 26-27

Related News

MOREMajor FMCG cities

- Chandigarh

- Maharashtra

- Tamil Nadu

- Gujarat

- Punjab

IBEF Campaigns

MORE

Aatmanirbhar Bharat Utsav 2024

Union Minister of External Affairs, Dr. S. Jaishankar and Union Commerce an...

Case Studies

MORESmart Metering Deployment in India Policy Framework, Institutional Structure and National Implementation Status

smart metering deployment in India, smart meter policy India, smart metering implementation India, smart meter rollout, institutional framework for sm...

How Digital Payments Are Enhancing Efficiency for Small Businesses in India

India’s digital payments ecosystem has emerged as a pillar of Micro, Small, and Medium Enterprises (MSMEs) economies. MSMEs in India are estimat...

Tourism in India Growing with Better Infrastructure and Richer Experiences

India has positioned itself prominently within the global tourism landscape. The country currently accounts for 1.40% of total international tourist a...

IBEF BLOG

MORE

Why India Is Emerging as a Global Hub for Biotechnology Innovation

The Indian bio sector has experienced notable transformation, and this incl...

Why Jute Products Are Important for Sustainable Packaging

The global packaging industry is undergoing a structural shift as businesse...

India’s Agri Value Chain Expansion through Nuts, Cocoa and Fisheries

The agricultural industry in India is at a stage where it is moving from th...

Partners