Market Spotlight: Gulf Cooperation Council

The Gulf Cooperation Council (GCC) is an intergovernmental organization comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates, which fosters cooperation in economic, social, and military fields. Established on May 25, 1981, in response to regional security concerns, today the organization commands significant oil reserves and has a strong presence in global trade flows.

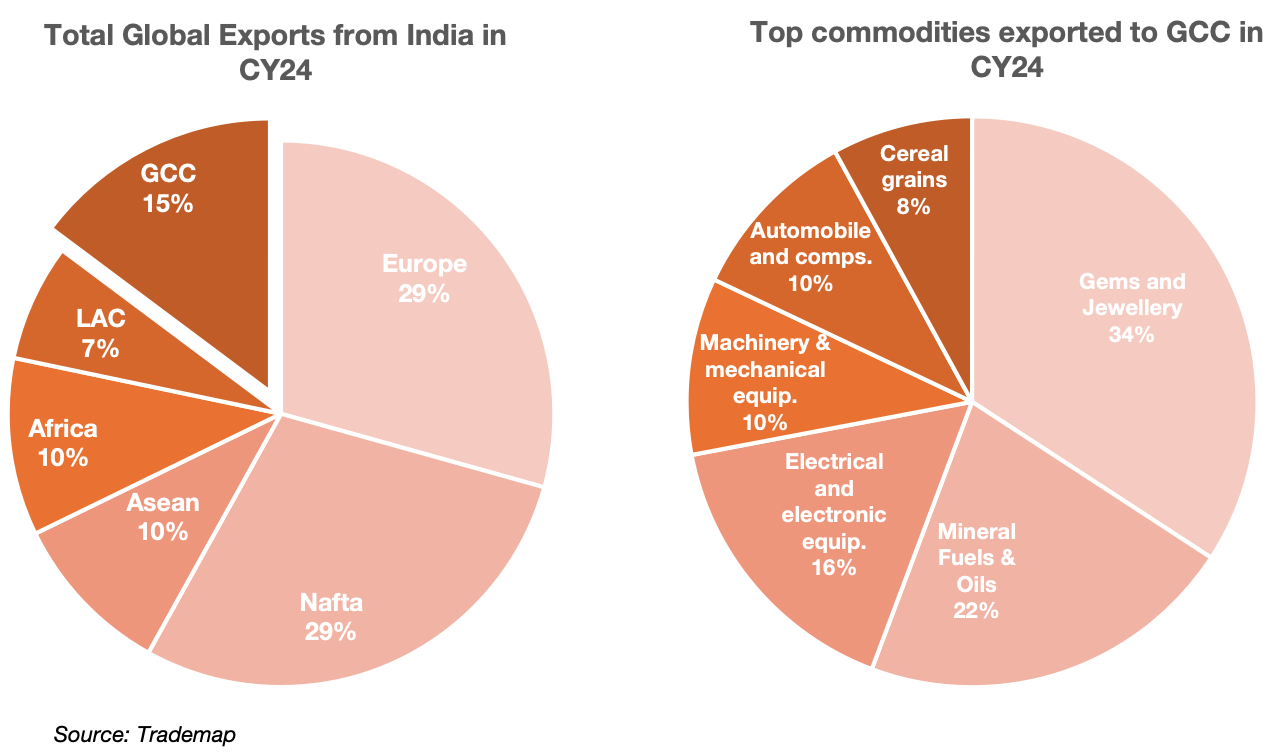

Collectively, GCC is strategically important to India. The region’s substantial oil and gas reserves play a vital role in supporting India’s energy needs. Trade relations have also been growing steadily. During CY24, exports from India to the GCC region stood at Rs. 4,89,894 crore (US$ 54.56 billion), representing 12.47% of India’s global exports. In the same period, bilateral trade between India and GCC reached Rs. 12,87,858 crore (US$ 143.43 billion).

Foreign Direct Investment (FDI) inflows from the GCC into India has also remained robust over the years, reflecting deep economic ties and sustained investor confidence. Cumulative investments from January 2000 to September 2025 reached Rs. 3,80,799 crore (US$ 42.41 billion) with UAE and Saudi Arabia contributing the highest FDI among GCC members. This underscores the growing role of the GCC in supporting India’s long-term growth, infrastructure development, and industrial expansion.

Competition Analysis:

India’s share in GCC imports has increased steadily from 5.88% in CY20 to 6.76% in CY24. China, United States (US), Japan and Germany are a few top GCC exporters with a 19.83%, 7.06%, 3.74% and 3.27% share, respectively. Gems and jewellery, mineral fuels and oils, electrical and electronic equipment and machinery and mechanical equipment continue to rank among India’s key exports to the GCC. These have been driven by competitive pricing, rising quality standards, established production strengths, and sustained demand from the region’s energy, infrastructure, trading, and industrial activities. India across these sectors competes with the following economies:

China: Historically, China’s engagement with Gulf countries has been anchored in energy ties. China has steadily deepened its economic presence in the region by emerging as a major importer of crude oil and a leading exporter of electronics, machinery and vehicles. Supported by competitive pricing and strong demand, China has become the largest trading partner of GCC, accounting for ~20% of the GCC’s total imports and remains India’s biggest competitor in the region.

Although China and GCC have pursued a free-trade agreement (FTA) since 2004, the pact remains unfinished due to Gulf concerns over low-cost Chinese imports and their impact on domestic industries. This delay creates an opportunity for India to deepen trade ties with the GCC, supported by its growing manufacturing base, ongoing trade talks, and its role as a trusted partner in the region’s diversification plans.

United States: The US is GCC’s second largest exporter and India’s closest competitor. The country contributed ~7.1% of GCC’s total imports in CY24 with machinery and mechanical equipment, vehicles and aerospace products being the top exports. Mineral fuels and oils, although declining, remain the leading export category from the GCC to the US.

Recent developments around the US 2025 tariff measures have reshaped global trade flows, with GCC facing limited direct impact due to its low export exposure to the US market. While higher tariffs have marginally raised costs for some non-oil exports, strong oil revenues, fiscal buffers and diversified trade links with Asia have helped GCC economies absorb the shock and maintain stability.

Japan: Historically anchored in energy security, Japan’s trade ties with the GCC have relied heavily on crude oil supplies from the region. Over time, this energy-focused relationship has expanded to include automobiles, machinery, electronics, raw materials and additional segments. In 2024, Japan contributed ~4% to the GCC’s total imports, positioning it as the fifth largest exporter to the region. While its share trails India’s by a wide margin, Japan has seen consistent growth in export values over the last five years.

Building on this momentum, Japan and the GCC have resumed negotiations on a comprehensive FTA, with the second round of talks held in July 2025. The proposed agreement aims to expand cooperation beyond energy into goods, services, investment, e-commerce and trade facilitation, and could provide preferential market access and regulatory clarity for businesses on both sides. If concluded, the FTA is expected to further strengthen Japan-GCC trade flows and support deeper integration across manufacturing and services sectors.

Germany: Germany is a key supplier of machinery, automobiles, mechanical equipment and pharmaceutical products to the region, supporting infrastructure development and industrial expansion across GCC economies. This makes Germany the GCC’s sixth-largest exporter, accounting for ~3% of the region’s total import value.

Germany maintains a strong lead in vehicles and machine equipment exports, whereas India currently underperforms. India’s export promotion schemes and cost competitive labour base provide an opportunity to close the gap and exceed Germany’s presence in these categories.

India holds a strong position in the GCC market as one of the region’s leading exporters. Its wide export base and steady performance have allowed India to stay ahead of many competitors and build a stable presence.

This position supports India’s role as a reliable trade partner and provides a foundation for sustained growth in the GCC. India’s enduring strengths are evident in the following key commodities, in which it continues to deliver solid performance.

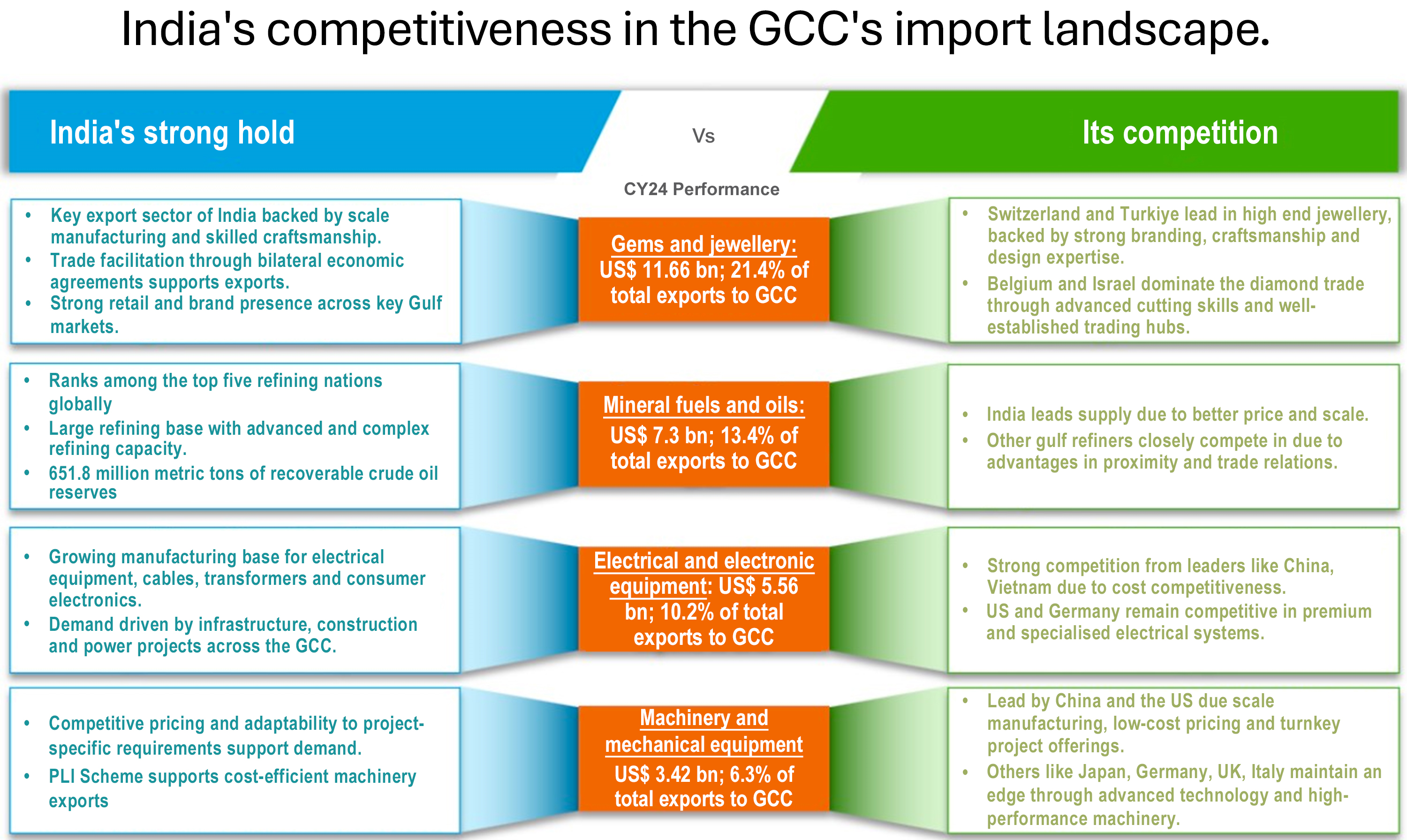

- Gems and jewellery - Gems and jewellery accounted for 21.4% of India’s total exports to the GCC, making India the third-largest exporter of this commodity to the region. Its export value increased to Rs. 1,04,699 crore (US$ 11.66 billion) in CY24 from Rs. 1,00,050 crore (US$ 11.14 billion) in CY23. Additionally, the India-Oman Comprehensive Economic Partnership Agreement (CEPA) abolishes customs duty on Indian gems and jewellery entering Oman, giving these products zero-duty access and significantly improving their price competitiveness in the Omani market. This move is expected to increase exports over the next few years starting from December 2026.

- Mineral Fuels & Oils - Mineral fuels and oils accounted for 13.4% of India’s total exports to the GCC. In CY24, India was the largest exporter followed by Saudi Arabia and Iraq. Export value increased from Rs. 34,582 crore (US$ 3.85 billion) in CY23 to Rs. 65,871 crore (US$ 7.34 billion) in CY24, a substantial 90.48% YoY increase. The sharp rise in India’s exports of mineral fuels, mineral oils and products of their distillation to GCC has been driven by high refinery throughput, strong overseas demand and India’s growing role as a refining hub.

- Electrical and electronic equipment - India saw a sharp rise in demand for electronic products in recent years. It now ranks as the world’s second largest mobile phone manufacturer. Electrical and electronic equipment accounted for a 10.2% share of India’s total exports to the GCC in CY24. Export values expanded significantly from Rs. 9,844 crore (US$ 1.10 billion) in CY15 to Rs. 49,932 crore (US$ 5.56 billion) in CY24, reflecting a 17.63% Compound Annual Growth Rate (CAGR) over the period. This strong performance has been underpinned by Production Linked Incentive (PLI)-led manufacturing scale-up and the Make in India initiative, with smartphones emerging as the primary driver of electronics export growth.

- Machinery and mechanical equipment - Machinery and mechanical equipment held 6.3% share of India’s total export into GCC. In terms of export value, the commodity grew from Rs. 24,069 crore (US$ 2.68 billion) in CY23 to Rs. 30,683 crore (US$ 3.42 billion) in CY24 showcasing a growth rate of 27.48% YoY. Currently, India stands as the ninth largest exporter of machinery and mechanical equipment into GCC with China, US, and Germany leading the pack. Furthermore, the India-Oman CEPA is expected to boost India’s machinery and mechanical equipment export to GCC by offering zero-duty access, improving competitiveness and supporting demand from ongoing infrastructure and industrial projects.

Other sectors gaining traction:

Automobiles and components: India’s automobile and auto components sector has emerged as a globally competitive manufacturing base, supported by large-scale production capacity, cost efficiency, and a well-integrated domestic supply chain. The sector benefits from strong participation of global original equipment manufacturers and a robust component ecosystem, enabling India to serve as a reliable export hub for vehicles and parts across international markets, particularly emerging regions such as the Gulf. Reflecting this strength, India ranked as the eighth largest exporter of automobiles and components to the GCC in CY24, accounting 4.4% of India’s total GCC imports in this category. Exports to the GCC increased from Rs. 6,632 crore (US$ 738 million) in CY15 to Rs. 30,575 crore (US$ 3.41 billion) in CY24, registering a CAGR of 16.53% over the decade.

Iron and steel products: Despite accounting for a modest 3.2% share, iron and steel product exports have risen steadily since 2020 and recorded a 23.2% value growth in CY24 compared with the previous year. In the same year, India stood as the second largest exporter of iron and steel products to the GCC. This growth is largely driven by demand from the GCC’s mega projects, along with India’s improving capacity to supply large volumes at competitive costs. India benefits from large scale manufacturing capabilities, abundant raw material availability and well-developed steel clusters, which lower overall production costs compared with many international markets where production and logistics expenses remain high.

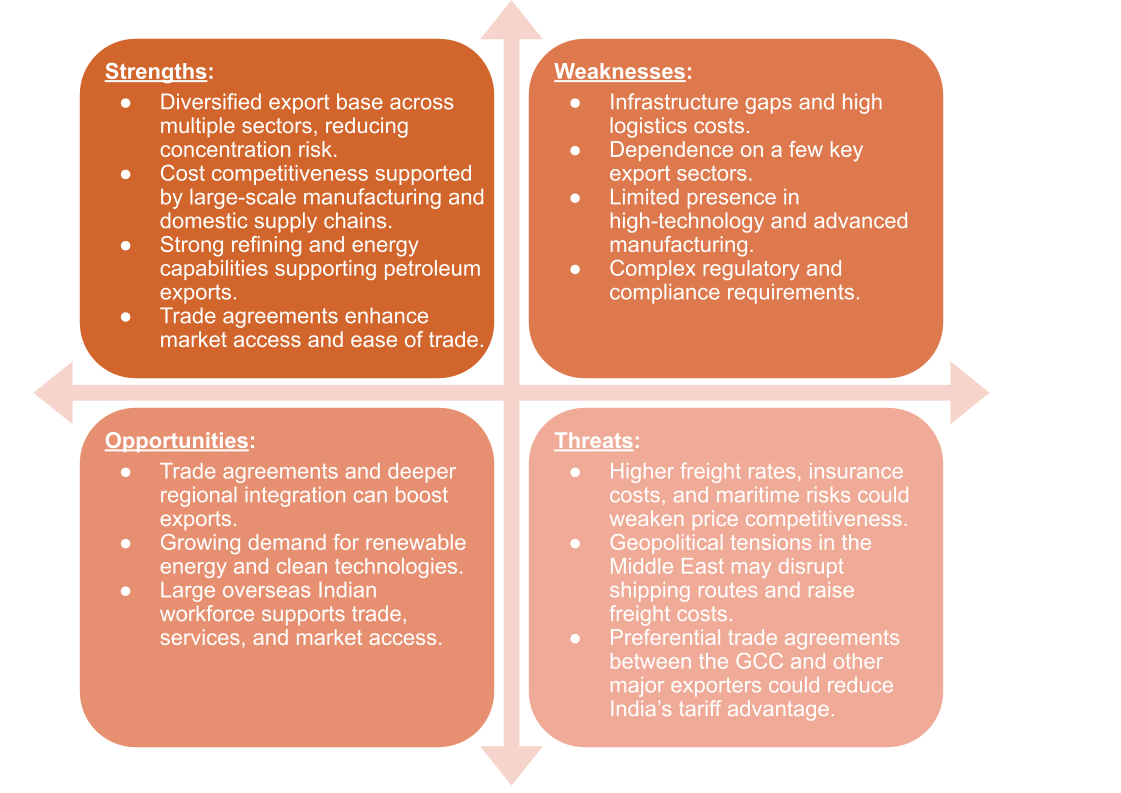

SWOT Analysis

Trade Agreements

India-GCC: Unlocking Trade Potential

India and the GCC are moving towards an FTA, with both sides finalising terms of reference to begin formal negotiations aimed at reducing trade barriers and expanding market access. While a broad GCC-India FTA is not yet in place, talks date back to a 2004 Framework Agreement and were renewed with intent to start formal discussions in 2025, reflecting the strategic importance of deep economic ties.

While a GCC-wide FTA with India is not yet in place, India has already advanced trade talks at an individual level within the Gulf by signing separate trade agreements, which are already improving market access and setting the groundwork for broader GCC-level engagement.

- CEPA - India and the India-United Arab Emirates CEPA, signed in May 2022, remains a central pillar of bilateral economic cooperation. The agreement covers trade in goods and services, investment, digital trade and intellectual property. It aims to reduce or eliminate tariffs on a large share of traded products while improving the ease of doing business. The CEPA provides faster customs clearance, simplified procedures and greater market access for businesses on both sides. Since its implementation, the agreement has been regularly reviewed to monitor progress and expand cooperation, with both countries working towards deepening trade ties and achieving higher non-oil trade levels in the coming years.

- India-Oman CEPA - In December 2025, India and Oman signed the India-Oman Comprehensive Economic Partnership Agreement (CEPA), granting zero-duty access on most tariff lines for both countries and enhancing trade in goods, services and investment. The pact aims to simplify customs procedures and boost market access for exporters, especially in key sectors such as engineering goods, chemicals, gems and jewellery, and textiles. By providing tariff advantages and strong economic cooperation, the India-Oman CEPA is expected to increase bilateral trade, support industrial growth and deepen commercial linkages between the two countries.

Actionable insights for Indian brands in the GCC

The GCC market is characterised by high purchasing power, strong import dependence, large scale infrastructure spending, and a young, digitally engaged population. Consumer preferences are shaped by quality, brand trust, convenience, and cultural alignment. Indian exporters can tap into the following opportunities:

- Value-for-Money with Quality Assurance: GCC consumers and institutional buyers prioritise quality, durability, and reliability but remain price conscious, especially in mass and mid-market segments. Backed by certifications and consistent quality, Indian brands can compete effectively by offering robust products at competitive prices. In the automobile, electrical equipment, and construction material sectors, Indian firms have gained traction by positioning products as cost-efficient alternatives without compromising on performance.

- Halal Compliance and Cultural Alignment: A halal certification is essential across food, beverages, cosmetics, pharmaceuticals, and personal care products in the GCC. Beyond certification, culturally sensitive branding, Arabic labelling, and alignment with local values enhance acceptance and trust. Indian companies with strong herbal, wellness, and pharmaceutical portfolios can gain an edge by proactively meeting halal and regulatory requirements.

- Premiumisation through Trust and Service: In high-income GCC markets, consumers are willing to pay a premium for trusted brands, strong warranties, and dependable after-sales service. Indian brands can move up the value chain by emphasising product longevity, service support, and lifecycle cost advantages, particularly in automobiles, appliances, and industrial equipment.

India-UK CETA: A Strategic Economic Re-Alignment

Marking a significant milestone in bilateral relations, India and the United Kingdom have signed the Comprehensive Economic and Trade Agreement (CETA) in July 2025. This deal marks a decisive shift from decades of lukewarm engagement to a fully institutionalised partnership. While previous interactions were governed by the 2021 Enhanced Trade Partnership (ETP), the new CETA is a binding roadmap designed to double bilateral trade by 2030. It reflects a clear strategic convergence: the United Kingdom’s post-Brexit "Global Britain" agenda needs a reliable growth engine, and India’s "Make in India" ambition needs a sophisticated G7 market. The India–United Kingdom partnership is anchored by this central pact, supported by critical side agreements on mobility.

- India-UK CETA - Signed during PM Modi’s visit to London in July 2025, this agreement is the heavy lifter of the relationship. It mandates the elimination of tariffs on over 90% of traded goods. For India, the immediate win is zero-duty access for 99% of its exports, giving a massive competitive boost to labour-intensive sectors like textiles, leather, and gems. In return, the UK gets access to the Indian market for its "iconic" exports: duties on Scotch whisky are slashed from 150% to 75% initially, and luxury automobiles see tariffs drop to 10% under a quota system. This isn't just about swapping goods; it's about integrating Indian manufacturers into British supply chains as the UK actively diversifies away from East Asian dependencies.

- Social Security Agreement (DCC) - Parallel to the main trade deal, the two nations operationalized a landmark Double Contributions Convention (DCC). This is a gamechanger for the services sector. It exempts professionals sent by their companies to the other country for temporary assignments from paying social security contributions in the host country for up to 36 months. For Indian IT giants like TCS and Infosys, this eliminates the unfair "dual burden" of paying into both UK National Insurance and the Indian Provident Fund, significantly lowering the cost of doing business in Britain.

Actionable insights for Indian brands in the UK

The UK market is characterized by a consumer base that is value-conscious but highly demanding of ethics and sustainability. Unlike the price-sensitive segments of emerging markets, the UK offers healthy margins for brands that can tell a compelling story and prove their "green" credentials. Indian exporters can tap into the following opportunities:

- Sustainability as a Differentiator: UK buyers are aggressively looking for "China Plus One" alternatives, but they won't compromise on environmental standards. In sectors like textiles, Indian manufacturers can leverage the new zero-duty access by doubling down on green production. Brands that can certify organic materials and low-carbon manufacturing will command a "green premium," positioning themselves not as cheap alternatives, but as ethical partners for British high-street retailers.

- Wellness and Heritage Branding: There is a real hunger for holistic health and natural beauty products in the UK. Indian brands in the Ayurveda space can replicate the success of companies like Forest Essentials by navigating the Traditional Herbal Registration (THR) scheme. The key here is moving beyond bulk exports of raw ingredients to selling finished, branded luxury goods. If you can package "Indian Heritage" with "UK Safety Compliance," there is a lucrative market waiting.

- Premiumisation of "Made in India": The CETA opens the door for high-value Indian manufacturing to enter the mainstream. Whether it's single malt whiskies like Amrut and Rampur gaining traction against local Scotch, or precision automotive components, there is a chance to shed the "low-cost" label. Indian firms should focus on establishing local after-sales support and warehousing in the UK to build trust, proving that Indian engineering offers both cost efficiency and global-grade reliability.

The India-EU FTA: Navigating the "Mother of All Deals" and a Multi-Trillion Dollar Pivot

The breakthrough at the 16th India-EU Summit in January 2026 has finally institutionalized one of the world's most significant trade corridors. Dubbed the "Mother of All Deals" by the press, this pact isn't just about shifting goods; it’s a massive strategic bet. By linking the world’s fastest-growing major economy with the largest single market, we are seeing a combined economic bloc of US$ 24 trillion, home to roughly 2 billion people, looking to insulate itself from global supply chain shocks and reduce over-reliance on single-source suppliers.

For the Indian exporter and the savvy investor, the agreement is built on three foundational pillars that will redefine business over the next decade.

- Market Access: The deal is remarkably lopsided in terms of immediate tariff relief, and that’s a huge win for Indian manufacturing. It mandates zero-duty access for over 99% of Indian exports by value. For the labour-intensive powerhouses (textiles, apparel, leather, and gems) this effectively removes the 4% to 26% tariff walls that previously hampered competitiveness.

- In exchange, India is opening its doors in a controlled, phased manner. We’re seeing a gradual climb-down of duties on 92.1% of EU tariff lines. This includes the "prestige" items: tariffs on European cars will eventually slide from 110% to just 10%, while the famously high 150% duty on wines and spirits will initially drop to 75% before settling at 20%.

- Services and the "Legal Gateway": Beyond physical goods, the agreement dives deep into 144 services subsectors, including IT, R&D, and professional consultancy. One of the most practical developments is the proposed "European Legal Gateway" office in India. This isn't just another bureaucratic layer; it's designed to be a streamlined hub for cross-border service delivery, making it much easier for Indian professionals to move and work on temporary assignments within the EU.

- The Trade and Sustainable Development (TSD) chapter: Perhaps the most "modern" part of this deal is the TSD. Unlike older trade pacts, this one is legally binding. It ties market access to environmental protection (Paris Agreement standards) and International Labour Organization (ILO) principles. It ensures that the growth we see isn't just fast, but ethical and sustainable, something the European consumer now considers a non-negotiable requirement.

Actionable insights for Indian brands in the EU

The European consumer is arguably the most sophisticated and demanding in the world. To really thrive under this FTA, Indian brands need to move past the "low-cost alternative" tag and embrace a "premium and compliant" identity.

- Secure the "Green Premium" :With the TSD chapter in effect, European retailers are scouring the globe for carbon-neutral and ethical supply chains. Indian textile and chemical firms that can prove circular economy practices or low-carbon footprints won't just get through the door; they’ll be able to charge a premium over less-compliant rivals.

- Monetize Heritage through TKDL : The agreement explicitly recognizes India’s Traditional Knowledge Digital Library (TKDL). This is a goldmine for Ayurveda and wellness brands. By combining centuries-old "Indian Heritage" with strict EU safety certifications, wellness players can target a high-margin market that is increasingly pivoting toward holistic health.

- Integrate into High-Tech Value Chains : The removal of duties (up to 14%) on electronics and components opens up an EU market worth $750 billion. Indian contract manufacturers, especially those in LED lighting and home appliances, should look at setting up European service hubs. The goal is to move from being a component supplier to a trusted brand that offers precision, reliability, and local support.

This FTA marks a "Viksit Bharat" milestone. The businesses that will win are those that treat this deal not just to save on duties, but as a mandate to upgrade their standards for a global stage.

The India-US Trade deal

Following the same strategic vein as the recent EU and UK agreements, the breakthrough announced in February 2026 between New Delhi and Washington marks a major pivot in the Indo-Pacific economic landscape. This isn't just a standard trade pact; it is a calculated de-escalation of what had become a punishing "tariff war." By slashing reciprocal duties and aligning on high-tech manufacturing, the two nations are essentially rewiring the supply chains of the future.

The India-US Interim Trade Agreement is built on following premises:

- Restoring Competitiveness: The headline-grabbing win here is the dramatic reduction of US tariffs on Indian goods, which have plummeted from a prohibitive 50% to a far more manageable 18%. This reset provides immediate oxygen to India’s labour-intensive powerhouses, which had been struggling under punitive levies.

Crucially, the deal moves toward zero-duty access for high-value segments like generic pharmaceuticals, gems, and aircraft parts. By removing these barriers, India isn't just selling more products; it’s positioning itself as the primary "China Plus One" manufacturing hub for a US market valued at over US$ 30 trillion. - The $500 Billion Energy & Tech "Buy-In": This agreement is underpinned by a massive $500 billion purchase intent over the next five years. India has committed to sourcing US energy (including coking coal), aircraft, and advanced technology products like Graphics Processing Units (GPUs) and data centre equipment. This isn't merely about balancing the trade deficit; it’s a strategic trade-off that secures India’s energy needs while integrating Indian tech firms into the high-end US semiconductor and digital infrastructure ecosystems.

- Calibrated Protectionism: One of the most impressive aspects of the deal is what isn't in it. Indian negotiators successfully ring-fenced the sensitive agricultural and dairy sectors. While India has eased access for US "premium" products like tree nuts, processed fruits, and spirits, it has granted no concessions on staples like wheat, rice, maize, poultry, or dairy. This ensures that the "Make in India" manufacturing surge does not come at the expense of the 720 million people dependent on India's rural economy.

Actionable insights for Indian brands in the US

The US market is the ultimate testing ground for scale. To win here, Indian firms need to look beyond the immediate 32% tariff relief and focus on deep integration.

- MSME Supply Chain Integration: With tariffs on machinery and components dropping to 18%, Indian MSMEs now have a window to become "tier-one" suppliers to American industrial giants. The focus should be on meeting US national security and quality standards, allowing firms to scale production from local clusters to global supply chains.

- The "Premium Artisanal" Play: The US consumer is increasingly shifting away from mass-produced East Asian goods toward "artisanal and heritage" products. Indian home décor and handicraft brands should leverage the new 18% rate to build branded presence in US high-street retail, moving from white-label manufacturing to high-margin consumer brands.

- Leveraging the Global Capability Centres (GCCs) Boom: While the H-1B visa landscape remains complex and costly, the "offshore delivery" model via GCCs in India is the real growth engine. Indian tech firms should double down on local talent delivery for US clients, bypassing physical mobility hurdles by providing high-end AI and R&D services directly from India.

The India-US deal has effectively ended the "Maharaja of Tariffs" era. The businesses that will thrive are those that can transition from being "low-cost exporters" to "strategic partners" in the world’s largest consumer market.

Disclaimer: This information has been collected through secondary research. The views expressed by the spokespersons are their own and do not necessarily reflect those of IBEF. IBEF is not responsible for any errors in the same.

Get In Touch

Your input is valuable in shaping the future of the IBEF Export Newsletter! Take a moment to share your thoughts and help us bring you more relevant insights, success stories, and export branding strategies.

Contact & Subscriptions: Contact Us

Email us at: info.brandindia@ibef.org

Call: +91 11 43845501

Partners