RECENT CASE STUDIES

Fuelling Growth: How India’s Petrochemical Industry is Powering Economic Transformation

Last updated: Aug, 2025

Petrochemicals are the unsung heroes of the modern industrial economy. Derived primarily from hydrocarbons such as natural gas and crude oil, these chemical compounds are the building blocks of countless products and industries. From plastic components in smartphones and medical equipment to synthetic textiles, fertilisers, detergents, automotive parts and packaging materials, petrochemicals are deeply embedded in our everyday lives. As global demand for consumer goods, infrastructure, healthcare and sustainable materials accelerates, the strategic importance of the petrochemical industry has increased significantly.

For India—a rapidly developing economy with ambitious growth targets—the petrochemical sector plays a pivotal role in fuelling industrial transformation. Positioned at the crossroads of energy, manufacturing and innovation, the industry supports the nation’s broader economic goals, including Make in India, Atmanirbhar Bharat (self-reliant India) and the National Infrastructure Pipeline. By enabling value addition across downstream industries such as construction, agriculture, textiles and transportation, petrochemicals enhance domestic productivity while reducing reliance on imports of finished goods.

India’s demographic dividend, rising middle-class consumption and expanding urban infrastructure are driving strong domestic demand for petrochemical-based products. Simultaneously, India is emerging as a viable alternative to China in global supply chains, offering cost competitiveness, a skilled workforce, and favourable policy incentives for petrochemical investment. Large, integrated petrochemical complexes and refining capacity expansions are further bolstering India’s potential to become a regional and global petrochemical hub.

However, this transformation is not without complexities. The petrochemical industry must simultaneously address environmental sustainability, energy-transition imperatives and the need for circularity in production and consumption. As India aims for net-zero emissions by 2070, the petrochemical sector stands at a critical inflection point—where economic opportunity intersects with environmental responsibility.

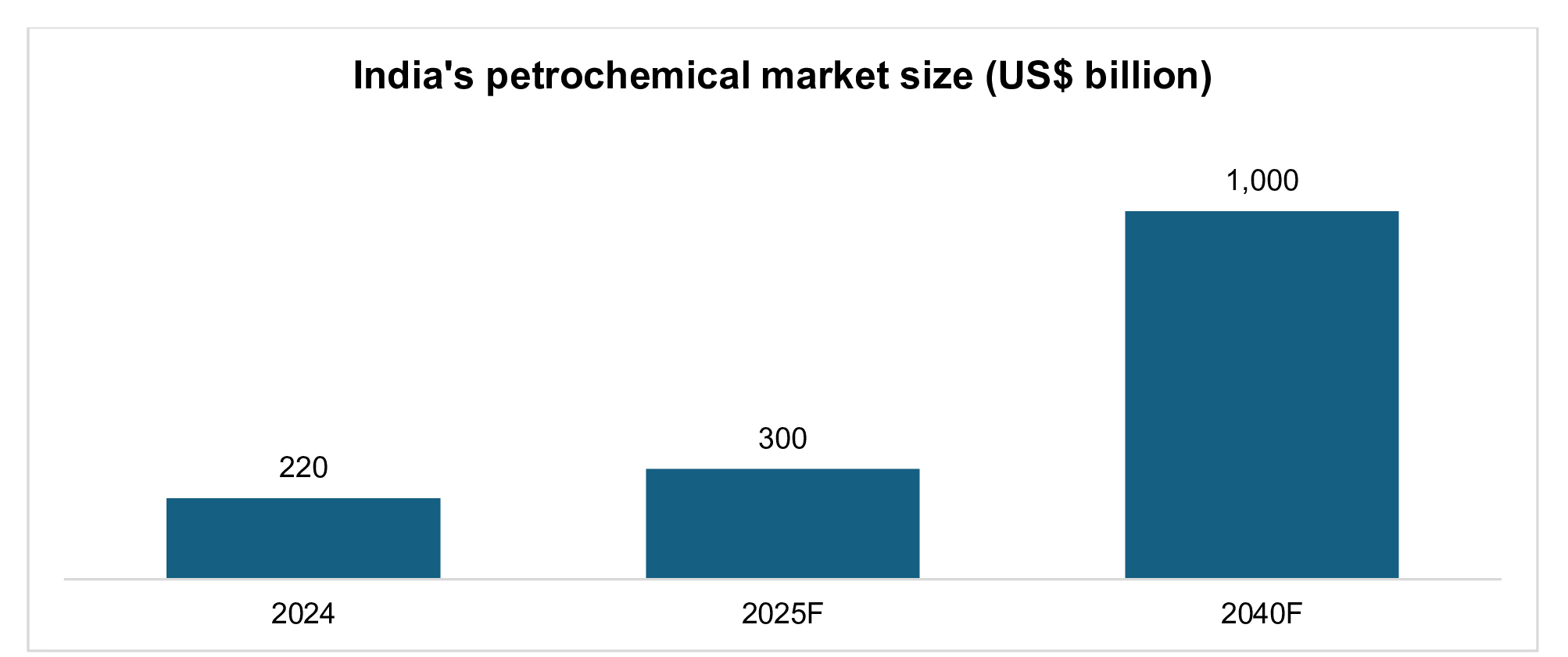

India’s chemical and petrochemical market

Source: PIB

India’s petrochemical industry has emerged as a cornerstone of the country’s industrial economy, with its market value reaching an estimated US$ 220 billion in 2024. This robust growth is being driven by surging domestic demand across sectors such as packaging, automotive, construction, agriculture, healthcare and textiles—all of which rely heavily on petrochemical derivatives like polymers, synthetic rubbers and specialty chemicals.

According to India’s Union Minister of Petroleum and Natural Gas, Mr. Hardeep Singh Puri, the market is projected to grow to US$ 300 billion by 2025, reflecting a compounded annual growth rate (CAGR) of 10–12% (2025-2040). This near-term growth is being catalysed by rising consumer consumption, infrastructure expansion under the National Infrastructure Pipeline (NIP) and an increased focus on import substitution under the Atmanirbhar Bharat initiative. Major capacity additions by leading players like RIL, IOCL and Haldia Petrochemicals Limited (HPL), along with government-backed projects in PCPIRs, are reinforcing India’s ability to scale production.

Looking ahead, the industry is poised for exponential expansion, with projections estimating the market to reach US$ 1 trillion by 2040. This transformation will be driven by structural shifts in global supply chains, with India emerging as a viable alternative to China for cost-competitive, high-volume production. Moreover, technological advancements, growing exports and a rising demand for green and sustainable alternatives are expected to further reshape the industry landscape.

India’s demographic dividend, expanding middle class and evolving industrial ecosystem place it in a unique position to become a global petrochemical powerhouse. Achieving the US$ 1 trillion milestone will require a cohesive strategy involving policy reforms, infrastructure investments, R&D incentives and a strong focus on sustainability—ensuring that economic growth goes together with environmental stewardship.

Types of petrochemical products: Building blocks of industrial growth

India’s petrochemical industry produces a wide range of essential chemicals that serve as the backbone of numerous downstream industries. These products are typically classified into basic petrochemicals and derivatives, with the most prominent categories being olefins, aromatics, polymers, synthetic fibres and fertiliser inputs.

- Olefins

Olefins are key building blocks in the petrochemical chain and include ethylene, propylene and butadiene. These are produced through the cracking of naphtha or natural gas and are primarily used to manufacture plastics, synthetic rubbers and solvents. Ethylene and propylene are also precursors for PE, polypropylene (PP) and PVC—compounds essential to the packaging, construction and automotive sectors.

- Aromatics

Aromatics such as BTX are derived from reforming processes in refineries. These chemicals are widely used in the production of dyes, detergents, synthetic fibres (like nylon and polyester), resins and adhesives. Aromatics also serve as key intermediates for several specialty chemicals and pharmaceuticals.

- Polymers

Polymers are the most visible output of the petrochemical industry and include PE, PP, PVC and polystyrene (PS). These materials are vital for making plastic packaging, pipes, automotive components, household goods, textiles and medical devices.

- Fertiliser Inputs

Petrochemical derivatives such as ammonia, urea and methanol are essential in the manufacturing of nitrogen-based fertilisers, which support India’s vast agricultural sector. These chemicals are often produced using natural gas as a feedstock.

- Others

Other important products include synthetic rubbers, acrylonitrile, ethylene oxide and glycols, which are critical for paints, coatings, cosmetics and industrial fluids.

Economic impact: Fuelling growth at scale

The petrochemical industry plays a critical role in India’s economic transformation, serving as a strategic enabler of industrial growth, employment generation and value chain development. With its deep linkages across core and consumer-facing sectors, petrochemicals significantly contribute to India’s GDP, industrial output and self-reliance initiatives.

Contribution to GDP and Industrial Output

India’s petrochemical sector is a major contributor to the manufacturing Gross Value Added (GVA) and overall GDP. The industry was valued at US$ 220 billion in 2024 and contributed ~6% to India’s GDP, underscoring its long-term importance in the country’s economic architecture. The sector contributes significantly to industrial production, both directly through chemical manufacturing and indirectly by supplying raw materials to multiple high-growth industries.

The integration of petrochemical production with refining and natural gas infrastructure further enhances operational efficiency and cost competitiveness. This vertical integration allows companies to capture more value across the chain, driving up margins and encouraging reinvestment into capacity expansion, R&D and sustainability initiatives.

Employment Generation: Direct and indirect

The petrochemical industry is also a significant employment generator. The petrochemical industry in India provides employment to approximately five million people. While direct employment in large-scale plants may be low due to automation and capital intensity, the indirect employment impact is significant. The sector supports a vast ecosystem of downstream industries, logistics providers, construction workers, engineering services, maintenance contractors and small & medium-sized enterprises (SMEs).

According to industry estimates, for every direct job in petrochemical manufacturing, six to eight indirect jobs are created across the logistics, processing, distribution and end-use industries. With the planned investments in mega petrochemical clusters such as PCPIRs, the employment multiplier effect is expected to grow substantially over the next two decades.

Moreover, the development of downstream clusters—particularly in states like Gujarat, Maharashtra, Odisha, Tamil Nadu and Andhra Pradesh—creates localised employment opportunities and helps in regional economic development.

Linkages with downstream industries

Petrochemicals serve as critical inputs for several downstream industries that together account for a significant share of India’s industrial output and exports. Key sectors include:

- Plastics & Packaging: Petrochemical derivatives such as PE, PP and PVC form the base of India’s packaging and plastic manufacturing industries. These are essential for the FMCG, pharmaceuticals, electronics and food processing sectors.

- Textiles & Apparel: Synthetic fibres like polyester, nylon and acrylic—derived from petrochemicals—are integral to the textile sector, especially in man-made fibre production, which supports India’s fast-growing fashion and export-oriented apparel industry.

- Automotive & Electronics: Engineering plastics, synthetic rubbers and specialty polymers are widely used in automobiles, electrical components and consumer electronics, helping reduce weight, improve durability and enhance energy efficiency.

- Construction & Infrastructure: PVC pipes, insulation materials, adhesives, paints and coatings—derived from petrochemicals—are vital to modern construction, plumbing and electrical systems.

- Agriculture: Fertiliser inputs like urea and ammonia, plastic mulching films, irrigation tubing and crop protection chemicals all depend on petrochemical feedstocks, boosting productivity in Indian agriculture.

These strong inter-sectoral linkages mean that growth in petrochemicals has a cascading impact on a wide range of other industries, magnifying its economic contribution.

Boosting domestic manufacturing and reducing import dependency

One of the most strategic roles of the petrochemical sector is its ability to strengthen domestic manufacturing and reduce dependence on imports of value-added products. India has historically been a net importer of several petrochemical derivatives, especially specialty chemicals, engineering plastics and high-performance polymers. However, with rising domestic capacity and investment in integrated complexes, the gap is steadily narrowing.

Government schemes such as Make in India, Production-Linked Incentive (PLI) for Chemicals and the development of PCPIRs are further incentivising backward and forward integration. These initiatives are enabling Indian companies to not only meet domestic demand but also emerge as competitive exporters of polymers, fibres and intermediates.

Furthermore, building domestic capacity in petrochemicals directly supports India’s ambition to become a global manufacturing hub. By ensuring the availability of essential raw materials at competitive prices, the industry enhances the competitiveness of downstream sectors such as electronics, textiles, auto components and medical devices.

Export potential and global competitiveness

India’s petrochemical industry has evolved from a domestic supplier to an emerging global contender in the chemicals and materials value chain. Backed by a robust refining base, competitive feedstock availability and strategic coastal infrastructure, India is increasingly tapping into global markets for petrochemical exports. As global supply chains diversify away from China, India’s potential to become a preferred alternative for petrochemical sourcing is gaining momentum.

Petrochemical exports: Key products, destinations and growth trends

India’s petrochemical exports include a wide range of basic and value-added chemicals such as polymers (PE, PP, PVC), synthetic rubbers, aromatics (BTX), styrene, glycols, ammonia, methanol and fertiliser intermediates. Indian producers like RIL, IOCL, HPL and OPaL have significantly expanded their export footprint in recent years.

Key export destinations include China, the UAE, Bangladesh, Vietnam, Turkey, Belgium, the US and Africa. Notably, India has also been increasing its share in the ASEAN and Latin American markets, where demand for low-cost, quality polymers and intermediates is growing rapidly. In FY24, India’s petrochemical exports were valued at over US$ 40 billion, with polymers and organic chemicals accounting for a major share. Despite global trade headwinds and pricing volatility, India’s petrochemical exports have maintained an upward trajectory due to strong demand in developing economies and competitive pricing.

India’s positioning in the global supply chain

India is strategically positioned to become a regional export hub for petrochemicals, given its:

- Geographical advantage: Proximity to key shipping routes and high-growth markets in Asia, the Middle East and Africa.

- Feedstock flexibility: Access to both naphtha- and gas-based crackers.

- Cost-effective manufacturing: Driven by economies of scale, integrated facilities and labour efficiency.

- Strong refining base: India is one of the largest exporters of petroleum products, which supports captive feedstock for petrochemical complexes.

Additionally, as global manufacturers diversify supply chains under the ‘China+1’ strategy, India is being viewed as a reliable partner for sourcing intermediates and specialty chemicals, especially considering rising Environmental, Social and Governance (ESG) compliance and geopolitical shifts.

Free Trade Agreements and trade policy enablers

India’s trade policy is increasingly aligned to support petrochemical exports through a network of Free Trade Agreements (FTAs) and bilateral arrangements. FTAs with countries and regions such as the UAE (CEPA), ASEAN and Japan, as well as ongoing negotiations with the EU, the UK and Australia offer opportunities to lower tariffs, streamline customs processes and improve market access.

The Remission of Duties and Taxes on Export Products (RoDTEP) scheme, PLI incentives for chemicals and customs duty rationalisation for raw materials have also enhanced the export competitiveness of Indian companies. Furthermore, policy clarity and proactive engagement in trade talks are helping Indian firms enter long-term contracts and joint ventures with overseas buyers.

Role of special and coastal economic zones

Special Economic Zones (SEZs) and Coastal Economic Zones (CEZs) have played a pivotal role in driving petrochemical exports. Facilities located in SEZs such as Dahej, Mundra, Jamnagar and Vizag benefit from duty-free imports, tax exemptions and world-class logistics infrastructure.

These zones are integrated with ports, allowing seamless export of high-volume cargo to global markets. The upcoming PCPIRs in states like Gujarat, Andhra Pradesh and Odisha are also being designed with export-oriented infrastructure, R&D hubs and plug-and-play industrial parks to attract global investors and companies.

India’s petrochemical industry stands at a pivotal juncture, poised to play a defining role in the country’s journey towards becoming a US$ 5 trillion economy. With demand for petrochemical products expected to surge across sectors like packaging, textiles, automotive and agriculture, the industry is projected to quadruple in size—from US$ 220 billion in 2024 to US$ 1 trillion by 2040. The government's push for domestic manufacturing, along with infrastructure investments in PCPIRs, SEZs and CEZs, is creating a fertile environment for growth. Simultaneously, the global pivot towards sustainable practices and supply chain diversification presents India with an opportunity to emerge as a competitive alternative to traditional petrochemical giants. As companies embrace ESG commitments, invest in green technologies and explore bio-based and circular economy models, the industry is evolving to meet both economic and environmental goals. Challenges related to feedstock dependency, infrastructure and regulatory frameworks persist, but they are being increasingly viewed as opportunities for innovation and strategic investment. Looking ahead, India’s petrochemical sector is not only expected to fuel industrial expansion but also to anchor the nation’s ambitions in clean energy, global trade and inclusive development. With the right policy support and collaborative efforts, the petrochemical industry can become a cornerstone of India’s economic transformation.

Partners