SEARCH

RECENT POSTS

Categories

- Agriculture (35)

- Automobiles (19)

- Banking and Financial services (35)

- Consumer Markets (55)

- Defence (6)

- Ecommerce (21)

- Economy (71)

- Education (13)

- Engineering (7)

- Exports (21)

- Healthcare (25)

- India Inc. (9)

- Infrastructure (30)

- Manufacturing (31)

- Media and Entertainment (16)

- Micro, Small & Medium Enterprises (MSMEs) (15)

- Miscellaneous (31)

- Perspectives from India (35)

- Pharmaceuticals (5)

- Railways (4)

- Real Estate (18)

- Renewable Energy (19)

- Research and Development (12)

- Retail (1)

- Services (6)

- Startups (15)

- Technology (64)

- Textiles (8)

- Tourism (14)

- Trade (6)

Authors

India Packaged Drinking Water Industry: Demand Trends and Market Outlook

- Mar 30, 2026, 16:45

- Consumer Markets

- IBEF

India’s packaged drinking water industry has become an integral part of the nation’s fast-moving consumer goods (FMCG) ecosystem, reflecting evolving lifestyles, rising health awareness, and the growing emphasis on safe and reliable hydration. What was earlier viewed as a situational or travel-related purchase has steadily transformed into a regular consumption product across homes, offices, educational institutions, transport hubs, and hospitality establishments. This shift is closely aligned with India’s broader socio-economic progress, including urban expansion, higher purchasing power, and increased preference for quality-assured food and beverage products.

The industry’s expansion has also been supported by the formalisation of food processing, the rapid spread of organised retail, and strong consumer trust in established brands. With offerings spanning affordable mass-market products to premium and mineral water variants, packaged drinking water today caters to a wide spectrum of income groups and usage occasions. Industry and government-linked analyses consistently highlight the sector’s stable growth pattern and strong long-term demand outlook across both urban and semi-urban India.

Market Outlook and Segmentation

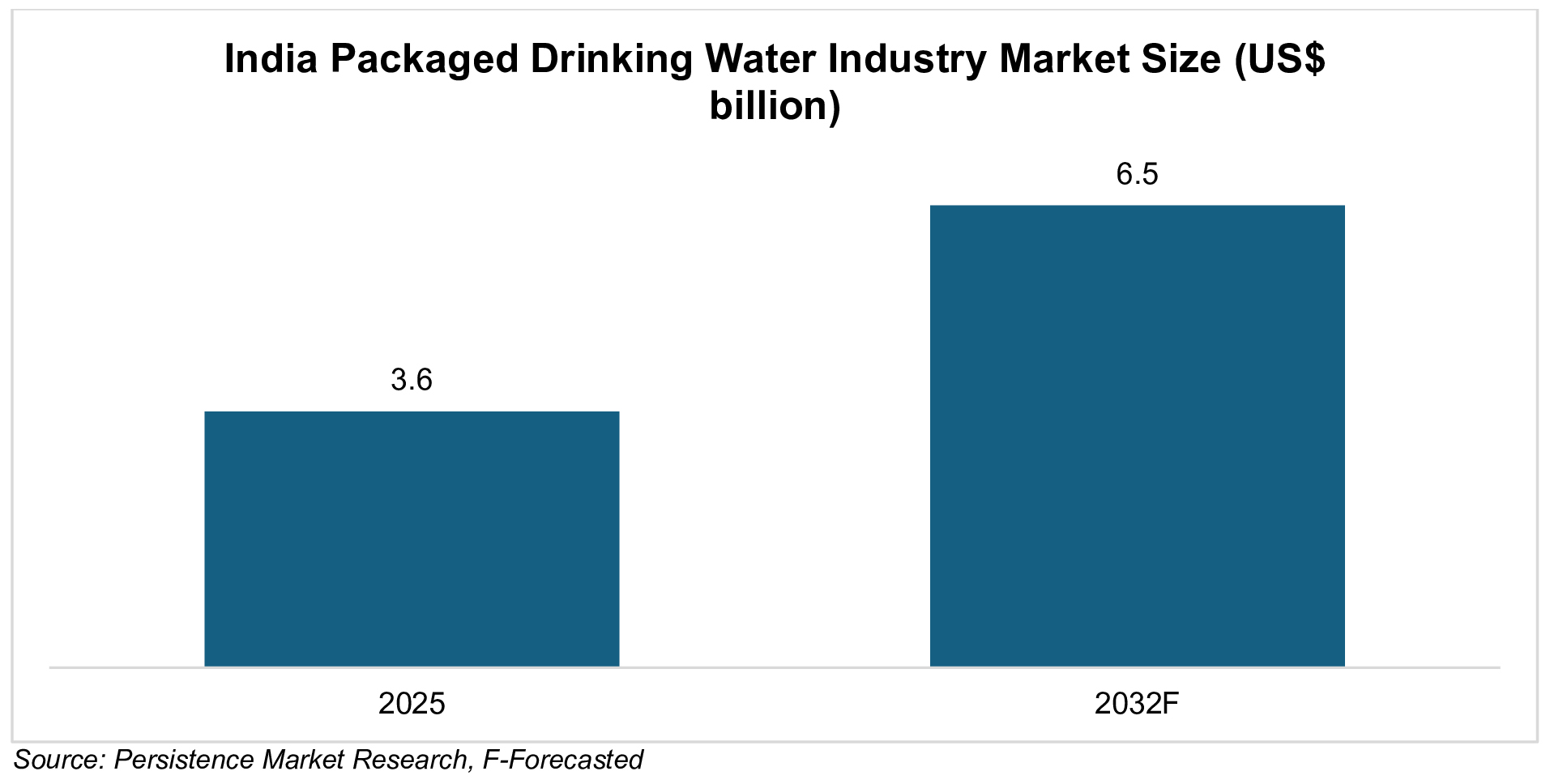

The India packaged drinking water market has demonstrated steady expansion and continues to show a positive long-term growth trajectory. The India packaged drinking water market size was valued at Rs. 32,040 crore (US$ 3.6 billion) in 2025 and is projected to reach value of Rs. 57,850 crore (US$ 6.5 billion) by 2032. This growth is underpinned by population growth, rising per-capita consumption, and increasing penetration of branded packaged water across diverse regions and consumer segments.

Further studies suggest that premium and mineral water categories are expanding faster than the overall market, driven by lifestyle positioning, rising disposable incomes, and demand from hospitality and institutional consumers. Market observers also recognise India as one of the most promising global markets for packaged drinking water, supported by its scale, climatic conditions, and rapidly developing retail and logistics infrastructure.

PET bottles dominate retail sales due to cost efficiency and ease of handling, while bulk jars (15–20 litres) are widely used in homes and institutions. Products are available in multiple pack sizes, 250 ml, 500 ml, 1 litre, 2 litres and bulk formats, allowing brands to cater to varied consumption occasions. By channel, off-trade sales accounted for over two-thirds of the market in 2024, while on-trade consumption through hotels, restaurants and cafes is expected to grow faster over the medium term, supported by tourism, hospitality recovery and rising out-of-home consumption. Regionally, North India held the largest share in 2024. These patterns influence where capacity is added and where investments in logistics and compliance readiness are concentrated.

Demand Trends Shaping Consumption

Multiple demand-side and supply-side factors are collectively shaping the growth trajectory of India’s packaged drinking water industry. Key drivers and emerging trends include:

Competitive Landscape

India’s packaged drinking water industry is characterised by a mix of large organised players and a wide base of regional and local manufacturers. While national brands command strong visibility and scale advantages, decentralised production and regional demand patterns have historically enabled the presence of numerous local operators across states and districts. This structure has resulted in a competitive but diversified market landscape.

Among organised players, Bisleri (Bisleri International Pvt. Ltd.) remains one of the most widely recognised brands, supported by an extensive pan-India distribution network across retail and institutional channels. Global beverage companies also maintain a strong foothold through their bottled water brands, including Kinley (Coca-Cola India Pvt. Ltd.) and Aquafina (PepsiCo India Holdings Pvt. Ltd.), particularly in modern trade, hospitality and large institutional supply.

Domestic brands such as Bailley (Parle Agro Pvt. Ltd.) continue to expand their presence across mass retail and bulk segments, leveraging established FMCG distribution networks. In parallel, emerging and premium-focused players such as Clear Premium Water (Clear Water Pvt. Ltd.) and Jeevsea Premium Water (Jeevsea Water Private Limited) are gradually scaling operations, particularly in urban retail, corporate consumption and bulk supply formats.

Policy and Compliance Framework

Policy and regulation play a central role in shaping the packaged drinking water industry, influencing product standards, sourcing practices and environmental responsibility.

Quality standards: Packaged drinking water is governed by specifications issued by the Bureau of Indian Standards (BIS). IS 14543 applies to packaged drinking water (other than natural mineral water), while IS 13428 governs packaged natural mineral water. Compliance with these standards underpins consumer trust and institutional procurement.

Groundwater regulation: Manufacturers sourcing groundwater are subject to guidelines issued by the Central Ground Water Authority (CGWA). These include requirements for No Objection Certificates (NOCs), monitoring and reporting, which increasingly influence plant location decisions and long-term operating continuity.

Plastic waste management: The Plastic Waste Management Rules, along with the strengthened Extended Producer Responsibility (EPR) framework, place responsibility on producers for collection, recycling and end-of-life management of plastic packaging. These requirements affect packaging choices, recycling partnerships and reporting systems, making sustainability a core operational consideration.

Food Safety and Standards Authority of India (FSSAI): The FSSAI governs packaged drinking water under its food safety regulations, prescribing standards related to composition, permissible limits, labelling and hygiene requirements. FSSAI’s framework ensures that packaged drinking water sold in India adheres to uniform safety and quality benchmarks, thereby reinforcing consumer confidence. The authority regularly issues guidance documents, training modules and compliance advisories for manufacturers, distributors and food business operators to maintain consistent standards across the value chain

The Road Ahead

The packaged drinking water industry in India is positioned for sustained growth, supported by rising consumption, expanding distribution networks, and increasing preference for branded hydration solutions. Continued penetration into emerging urban centres, product diversification, digital channel expansion, and strong institutional demand are expected to reinforce the sector’s momentum. As consumption patterns evolve, packaged drinking water is set to further strengthen its role as an essential and trusted FMCG category within India’s growing consumer economy.

FAQs

What is the current market size of India’s packaged drinking water industry?

The market was valued at Rs. 32,040 crore (US$ 3.6 billion) in 2025 and is projected to reach Rs. 57,850 crore (US$ 6.5 billion) by 2032, supported by rising consumption and wider brand penetration.

Which segment dominates the packaged drinking water market in India?

Mass packaged drinking water sold in PET bottles and bulk jars dominates in volume terms, with off-trade retail accounting for over two-thirds of total sales.

What are the key growth drivers of the packaged drinking water industry in India?

Key drivers include health and hygiene awareness, urbanisation, strong retail and kirana distribution, and rapid growth of e-commerce and quick commerce platforms.

How is the packaged drinking water industry regulated in India?

The industry is regulated by BIS quality standards and FSSAI food safety norms, along with groundwater guidelines from CGWA and plastic waste management rules.

Which companies dominate India’s packaged drinking water market?

Bisleri is the most widely recognised brand, followed by Kinley and Aquafina, with several domestic and premium brands expanding their presence.

Partners