SEARCH

RECENT POSTS

Categories

- Agriculture (35)

- Automobiles (20)

- Banking and Financial services (35)

- Consumer Markets (55)

- Defence (6)

- Ecommerce (21)

- Economy (72)

- Education (13)

- Engineering (7)

- Exports (21)

- Healthcare (25)

- India Inc. (9)

- Infrastructure (30)

- Manufacturing (31)

- Media and Entertainment (16)

- Micro, Small & Medium Enterprises (MSMEs) (15)

- Miscellaneous (31)

- Perspectives from India (35)

- Pharmaceuticals (5)

- Railways (4)

- Real Estate (18)

- Renewable Energy (19)

- Research and Development (12)

- Retail (1)

- Services (7)

- Startups (15)

- Technology (65)

- Textiles (8)

- Tourism (14)

- Trade (6)

Authors

Pharmaceutical Companies in India Advancing Innovation and Global Reach

- Mar 12, 2026, 11:30

- Pharmaceuticals

- IBEF

India’s pharmaceutical sector is transitioning into a phase of capability-led and innovation-driven growth. While large-scale manufacturing remains the foundation of its global relevance, the industry is increasingly strengthening its position across research, advanced therapies and integrated global operations. India is the third-largest pharmaceutical producer globally by volume, a position built on decades of scale, regulatory alignment and cost competitiveness. Building on this base, pharmaceutical companies in India are moving beyond a pure supply-oriented role towards broader participation across research, development and manufacturing value chains.

Indian manufacturers are emerging as globally integrated players with expanding capabilities in complex formulations, biosimilars, vaccines, active pharmaceutical ingredients (APIs) and contract manufacturing services. This evolution has been enabled by scale efficiencies, strong regulatory compliance and sustained policy support.

Strategic Importance of Pharmaceutical Companies in India

India’s role in global healthcare has long been shaped by its leadership in generic medicines. Accounting for around 20% of global generic drug supply by volume, the country continues to play an important role in expanding access to affordable treatments, particularly across emerging and low-income markets. The industry has a deep and diversified base, comprising more than 3,000 pharmaceutical companies, over 10,500 manufacturing units, and more than 60,000 generic brands across nearly 60 therapeutic areas. A key competitive advantage for Indian pharmaceutical companies is their strong compliance with global quality standards. India hosts the largest number of US Food and Drug Administration (USFDA)-approved manufacturing facilities outside the United States, enabling reliable access to highly regulated markets. As a result, over 60% of India’s pharmaceutical exports are directed to stringent regulatory destinations, underscoring international confidence in India’s manufacturing ecosystem.

Indian pharmaceutical companies are increasingly redirecting capital and research efforts towards segments that require greater scientific depth and regulatory sophistication. Complex generics, biosimilars and biologics are becoming priority areas, especially in therapeutic categories such as oncology, immunology and chronic diseases. These segments are characterised by longer development timelines, higher entry barriers and specialised manufacturing capabilities.

Alongside this shift, India has strengthened its position in contract research, development and manufacturing organisation (CRDMO) services. Indian CRDMO players are engaging earlier in the global drug development lifecycle, supporting clinical research, process optimisation and scale-up manufacturing. This earlier involvement enables companies to build deeper technical expertise while aligning more closely with global innovation pipelines.

Market Landscape and Company Revenue

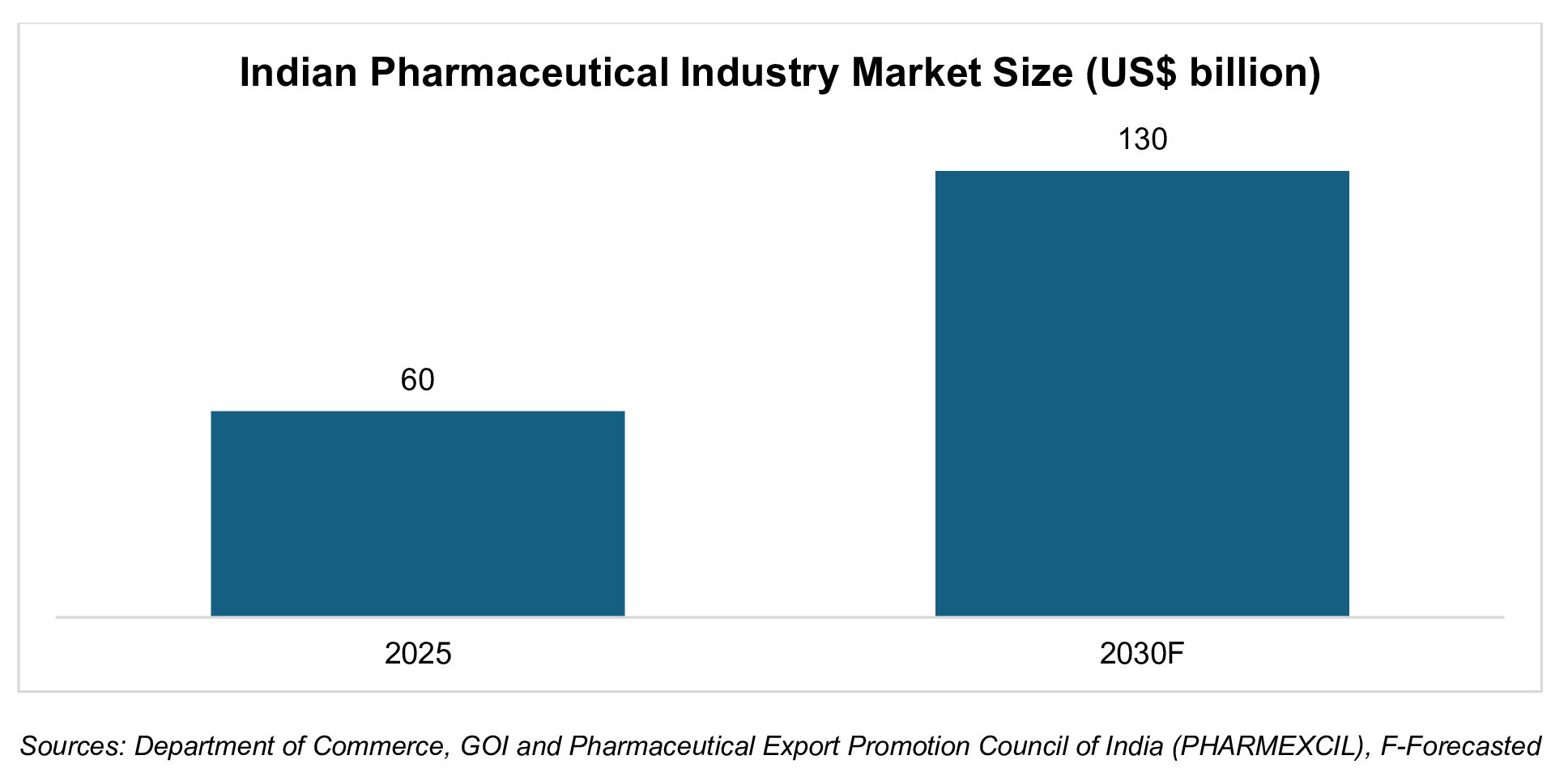

The Indian pharmaceutical industry was valued at Rs. 5.41 lakh crore (US$ 60 billion) in 2025 and is estimated to reach Rs. 11.73 lakh crore (US$ 130 billion) by 2030.This growth was driven by a balanced contribution from both exports and domestic consumption, rising life expectancy, increasing prevalence of non-communicable diseases such as diabetes and cardiovascular disorders, and improved access to healthcare services. India’s pharmaceutical exports stood at Rs. 2.71 lakh crore (US$ 30.47 billion) in FY25, registering a growth of 9.4% over the previous year supported by recovery in regulated markets, easing pricing pressures and higher approvals for complex generics.

India’s pharmaceutical industry continues to demonstrate strengthening profitability and solid financial health, reflecting the sector’s ability to adapt to changing cost structures and evolving market demand. An assessment of the top 50 listed and unlisted pharmaceutical companies indicates a steady improvement in operating performance following a temporary cost-led moderation in FY23. By FY25, the sector’s profit before interest, lease, depreciation and tax (PBILDT) margin had improved to approximately 23.40%, supported by easing raw material and freight costs, improved operating leverage and a favour

able shift towards higher-value products. The growing contribution from complex generics, speciality formulations and contract research and manufacturing services (CRAMS) is expected to support further margin expansion in upcoming years.

Global Reach Anchored in Compliance and Reliability

India’s global pharmaceutical footprint extends to more than 200 countries, spanning regulated, semi-regulated and emerging markets. This reach is underpinned by long-term investments in quality systems, inspection readiness and compliance with multiple international regulatory frameworks.

India’s position as the country with the largest number of US FDA-approved pharmaceutical manufacturing facilities outside the United States has become increasingly significant as global healthcare systems prioritise reliability, traceability and consistent supply. In addition, Indian manufacturers play a strategic role in global vaccine supply, accounting for over 55% of vaccines procured by UNICEF, reinforcing India’s contribution to global public health initiatives.

Several Indian pharmaceutical companies have established sustained international operations, supported by diversified portfolios and consistent exposure to regulated markets such as Sun Pharmaceutical Industries Limited, Cipla Limited, Divi’s Laboratories Limited, Dr. Reddy's Laboratories Limited, Zydus Lifesciences Limited, Mankind Pharma Limited, Ajanta Pharma Limited, Torrent Pharmaceuticals Limited, Lupin Limited. among others. Collectively, these companies are becoming more deeply embedded in global pharmaceutical value chains through research collaboration, technology transfer and advanced manufacturing, extending their role beyond exports into co-development and long-term partnerships.

Innovation Ecosystems Enabling Global Integration

India’s expanding innovation capacity is closely linked to the development of specialised pharmaceutical and biotechnology hubs. Cities such as Hyderabad, Bengaluru, Pune and Mumbai have evolved into integrated ecosystems where research, clinical development and manufacturing intersect.

India’s biotechnology landscape includes over 2,600 biotech start-ups, with Bengaluru emerging as a key centre for pharmaceutical and life sciences innovation. These hubs benefit from proximity to academic institutions, clinical research organisations and regulatory expertise, enabling faster translation from research to commercial production.

Infrastructure-focused initiatives, including the Scheme for Promotion of Bulk Drug Parks, support shared facilities such as testing infrastructure, effluent treatment plants and quality systems. By reducing compliance costs and improving operational efficiency, these initiatives strengthen India’s ability to meet international quality benchmarks and support export-oriented manufacturing.

Instead of operating in isolation, these ecosystems increasingly enable cross-border research collaborations, co-development efforts and technology transfer, helping India integrate more deeply into global pharmaceutical value chains.

Policy Environment Supporting Innovation and Global Integration

The Government of India has implemented a set of favourable policy measures to directly support pharmaceutical companies by strengthening manufacturing capabilities, quality infrastructure and long-term competitiveness. The Strengthening of Pharmaceutical Industry (SPI) scheme, with an outlay of Rs. 500 crore (US$ 60.9 million), provides targeted assistance to pharmaceutical clusters and MSMEs to enhance productivity, upgrade quality standards and promote sustainable manufacturing. This is complemented by the Scheme for Development of the Pharma Industry, an umbrella framework that supports companies through common facilitation centres, cluster development initiatives and technology upgrade assistance.

A significant policy push has been provided through the Production Linked Incentive (PLI) scheme, announced in September 2020 with a total outlay of Rs. 15,000 crore (US$ 2.04 billion), which incentivises pharmaceutical companies to expand domestic manufacturing of key starting materials, drug intermediates and active pharmaceutical ingredients. Within this, Rs. 6,940 crore (US$ 838.16 million) has been earmarked for the production of 41 bulk drugs during FY21 to FY30.

These measures are reinforced by increased allocations in the Interim Budget FY25 for bulk drug parks, pharmaceutical and medical device infrastructure, alongside innovation support through BIRAC and the PRIP scheme, approved with an outlay of Rs. 5,000 crore (US$ 604.5 million), collectively enabling pharmaceutical companies to scale innovation and expand their global footprint.

The Road Ahead

The next phase of growth for India’s pharmaceutical industry will be shaped by the adoption of technology and deeper international collaboration. Digital tools are being increasingly applied across drug discovery, clinical trials, and supply chains, improving efficiency, transparency, and regulatory compliance.

At the same time, partnerships with global pharmaceutical companies, research institutions and healthcare ecosystems are becoming more central to innovation strategies. As global healthcare ecosystems place greater emphasis on supply reliability and collaborative innovation, Indian pharmaceutical companies are increasingly being engaged not only as suppliers but also as development and manufacturing partners across global value chains.

FAQs

What is driving innovation in India’s pharmaceutical sector?

Investment in complex generics, biosimilars, biologics and CRDMO services is enabling higher-value growth and deeper global integration.

Why are global pharmaceutical companies partnering with Indian firms?

India offers a combination of scale, regulatory compliance, cost efficiency and technical expertise across manufacturing and development.

What is the current market size of India Pharmaceutical Industry?

The Indian pharmaceutical industry was valued at Rs. 5.41 lakh crore (US$ 60 billion) in 2025 and is estimated to reach Rs. 11.73 lakh crore (US$ 130 billion) by 2030.

How does government policy support global competitiveness?

Policy initiatives such as the pharmaceutical PLI scheme incentivise advanced manufacturing and innovation-led production.

What is the medium- to long-term outlook for the sector?

Sustained growth driven by innovation, advanced manufacturing and deeper integration into global pharmaceutical value chains.

Partners